- Why are foreclosure filings climbing across North Texas?

- What does home equity change when you’re behind?

- The five exits, and how much control each one leaves you

- 1. Sell the house at a price that moves

- 2. Short sale, when the debt outweighs the likely price

- 3. Loan modification, when the house is still affordable long term

- 4. Forbearance or a repayment plan, when the setback has an end date

- 5. Deed in lieu, when there’s no path back

- The options national guides add, and who they fit

- What happens to the leftover debt after the house is gone?

- Short Sale When the Mortgage Is Higher Than the Likely Sale Proceeds

- Loan Modification and Forbearance When the Home Is Still Affordable Long Term

- Deed in Lieu When Preserving Ownership Is No Longer Realistic

- When Waiting Too Long Removes the Best Options

- Texas Timelines Move Fast

- The Warning Signs That Usually Mean Choices Are Shrinking

- Why Agents and Investors Should Pay Attention Too

- A Practical Next Step for Homeowners in Trouble

- Answers to Common Questions About Foreclosure Alternatives in Texas

- Can I stop an auction that’s already scheduled?

- How much does each exit hurt my credit?

- Do I owe income tax if my lender forgives part of the debt?

- The Best Option Is Usually the One Chosen Early

Foreclosure filings are up sharply in North Texas. More than 2,700 properties in Collin, Dallas, Denton, and Tarrant counties entered foreclosure in the first four months of 2026, about a third more than the same period last year. Our phones show it. The owner on the other end usually assumes the house is already gone.

The house usually isn’t gone. Foreclosure alternatives are the exits available between a missed payment and the courthouse auction, and Texas law leaves room for five main ones. You can sell the home, arrange a short sale, rework the loan, pause payments under a forbearance plan, or hand back the title through a deed in lieu.

Which exits stay open depends on two things, your equity and the calendar.

| Option | Fits when | You keep | Watch for | Clock |

|---|---|---|---|---|

| Traditional sale | Home is worth more than the debt | Control of price and timing, plus cash left after payoff | Net sheet must clear the payoff before the sale date | 21 days minimum once the sale posts |

| Short sale | Debt runs higher than the likely price | A negotiated exit and softer credit damage | Deficiency waiver must be in writing | Lender approval runs 90 to 120 days |

| Loan modification | Income dropped, then recovered | The house | Approval is never promised | Apply before the file reaches the lender’s attorney |

| Forbearance or repayment plan | Short setback with an end date | The house, for now | The shortfall comes due later | Weeks to arrange |

| Deed in lieu | No path back to affordability | An exit without an auction | Debt treatment must land in writing | Lender must accept |

Why are foreclosure filings climbing across North Texas?

A McKinney family we met this spring had never missed a payment until their escrow rose $400 a month. Taxes and insurance did that on their own (the loan never moved). Multiply that household by a few thousand and you have the current county docket.

Call it a payment problem. Escrow problem is closer, since the note stayed exactly where it started and the bill grew anyway.

ATTOM counted 40,355 U.S. properties with foreclosure filings in May 2026, up 14% from a year earlier, and Texas led the country in foreclosure starts. The state logged 3,154 starts in April alone, most of them in the big metros. Slower resale traffic compounds the squeeze, with listing inventory in the major Texas metros running about 53% above normal levels, so a house that must close before an auction date sits longer than its owner can afford.

None of this repeats 2008. That wave came from loans that were bad on day one, while today’s defaults sit on top of real value. Jessica Lautz at the National Association of Realtors puts typical owner equity growth near 50% over the past five years, and that value changes which exits stay open.

How fast does the Texas foreclosure clock run?

Faster than almost anywhere. Texas foreclosures run without a courtroom, and the average Texas case in 2025 finished in roughly 135 days, though contested files run longer. ATTOM’s national average for completed foreclosures sat at 815 days in mid-2024. Plan around the national number and you lose exits you still had.

Four fixed marks control the schedule.

- Federal servicing rules block the first foreclosure filing until you’re more than 120 days behind (12 C.F.R. § 1024.41).

- The lender sends a notice of default and intent to accelerate, and you get 20 days to cure (Texas Property Code § 51.002).

- After acceleration, a notice of sale posts at least 21 days before the auction.

- The sale happens on the first Tuesday of the month at the county courthouse. Your attendance changes nothing.

One more Texas wrinkle. Once a trustee sale on a home loan closes, no general right of redemption exists, so the sale is final the day it happens. If you hope to stop a foreclosure, you have to act inside those windows.

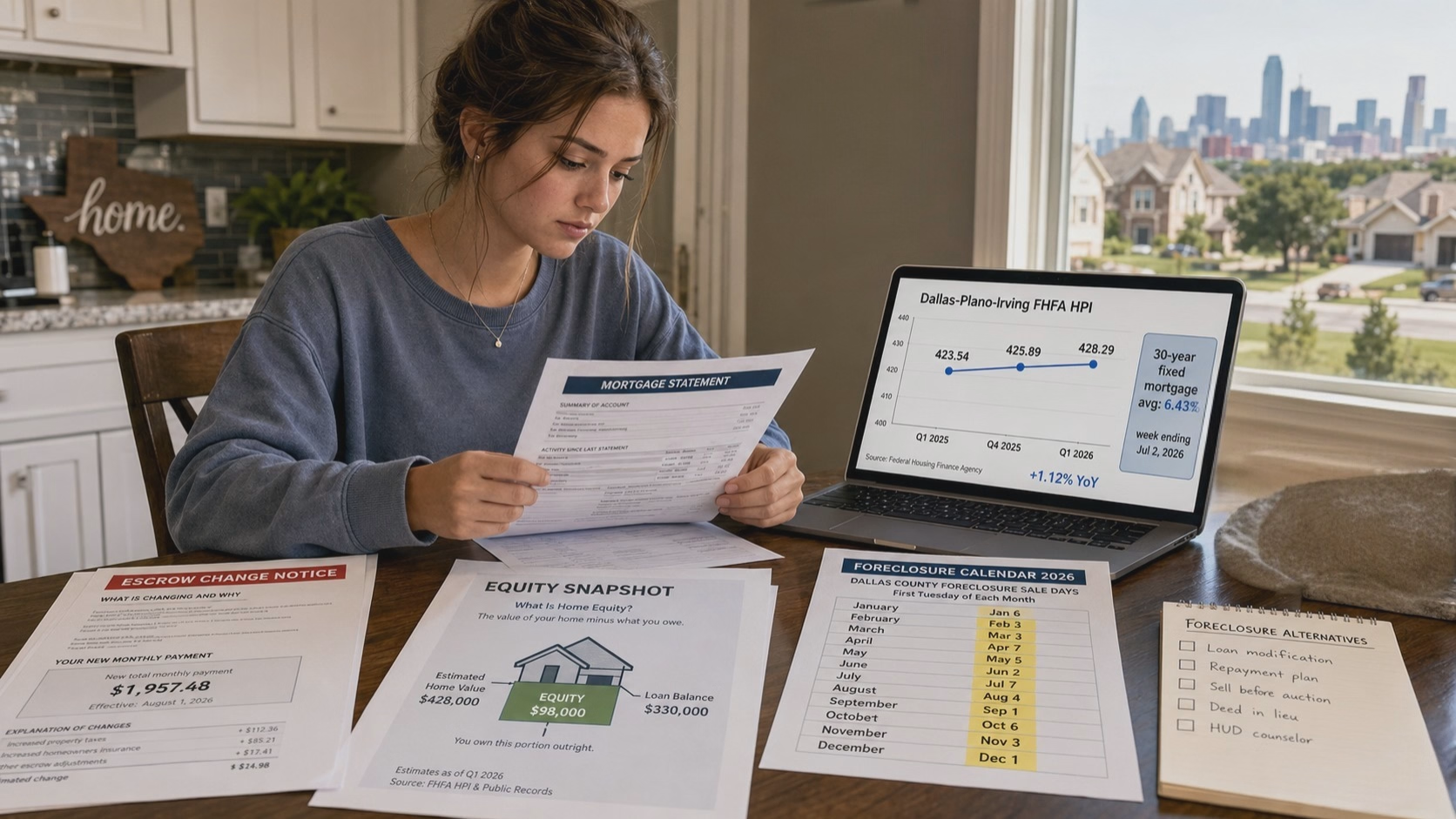

What does home equity change when you’re behind?

Almost everything. Equity is your home’s market value minus the loan payoff and the cost of selling. With it, you can list the house, pay the lender in full, and leave with cash. Without it, every exit needs the lender’s signature.

Gross equity isn’t the check you take home, though. Commissions, property taxes, repairs, liens, and missed-payment arrears all come out first, so ask your agent for a net sheet that itemizes each line. We’ve watched sellers overestimate their walk-away number by $40,000 (a real file, last winter) because the arrears never made it into the math.

The value also shrinks while you wait. Late fees, legal costs, and tax penalties stack up each month once payments stop, and a crowded market can force a lower list price at the same time. You can sit on five years of appreciation and still reach the auction with nothing if the file goes untouched.

That equity doesn’t make the problem disappear, but it does change the range of available exits.

The five exits, and how much control each one leaves you

1. Sell the house at a price that moves

When the home is worth more than the debt, a regular listing beats every lender-run process we’ve seen. Price it under the comps, because you’re selling against a deadline. Your equity absorbs the discount, your loan gets paid in full, and your credit damage stops at the late payments already reported.

The practical reality is you need the full runway of days between listing and closing. A financed buyer takes 30 to 45 days to close, so a listing that starts after the sale posting has almost no margin. Start before the notice if you can.

2. Short sale, when the debt outweighs the likely price

In a short sale, the lender agrees in writing to accept sale proceeds below the loan balance. Approval averages 90 to 120 days, and some files stretch toward a full year, so this exit rewards early movers.

The credit math favors it too. A short sale usually costs 50 to 150 points, against 100 to 160 for a completed foreclosure, and it trims the wait for your next mortgage to 2 to 4 years instead of 3 to 7. We put one condition on every short sale we touch. The deficiency waiver goes into the approval letter or the deal doesn’t close.

3. Loan modification, when the house is still affordable long term

A loan modification reworks the note permanently, usually with a longer term and sometimes a lower rate. Fannie Mae and Freddie Mac loans carry a named program for this, the Flex Modification, and FHA loans run their own loss mitigation menu. Apply early. Files that reach the lender’s attorney first face longer odds and higher fees.

4. Forbearance or a repayment plan, when the setback has an end date

Payments pause or shrink for a few months, then the shortfall gets repaid on top of the regular note. That structure fits a layoff with offers pending or a medical leave with a return date. Forbearance won’t fix a payment that was never affordable, and the deferred balance comes due either way.

5. Deed in lieu, when there’s no path back

You transfer title to the lender and skip the auction, and some lenders add relocation money to close the file. Two cautions. Get the debt treatment in writing before you sign anything. And ask a tax professional about the forgiven balance, since the IRS can call it income.

The options national guides add, and who they fit

HUD and the legal reference sites list a longer menu than the five above. Most of the extras fit narrow cases, which is exactly why they’re worth checking before you choose.

- A refinance can fold the arrears into a new loan. You need remaining equity and a credit score that still qualifies, which is rare past the second missed payment.

- FHA borrowers can request a Partial Claim, an interest-free loan that reinstates the mortgage and gets repaid when the house sells or the loan pays off.

- A mortgage assumption hands your loan, at its existing rate, to a buyer. Due-on-sale clauses block most of these. Federal law protects certain family transfers, including inheritance, divorce, and a spouse taking over the note after a death.

- Owners 62 and older sometimes hear about a reverse mortgage as a rescue, and we rarely point clients there because the equity cost runs high and reverse mortgages can foreclose too.

- Chapter 13 bankruptcy triggers a court-ordered stay that halts a scheduled sale and folds the arrears into a 3-to-5-year plan. The heaviest tool on this list, and those cases belong with bankruptcy counsel.

What happens to the leftover debt after the house is gone?

Texas gives lenders two years to sue for a deficiency, the difference between what you owed and what the sale brought (Texas Property Code § 51.003). The same statute hands you a defense. If the home sold below fair market value, a court can offset the shortfall by the difference.

What beats the statute? Paper. A short sale approval or deed-in-lieu agreement should say, in plain terms, that the lender releases the remaining balance, because verbal assurances from a servicer rep carry no weight later.

Have Texas real estate attorney read the waiver language before you close, and know your rights after foreclosure in case the sale already happened.

Using a moving home checklist can also help homeowners streamline their exit once the property goes under contract, minimizing last-minute delays that could push past a critical date.

Short Sale When the Mortgage Is Higher Than the Likely Sale Proceeds

When a lender officially consents to a settlement amount below the remaining loan balance, it is known as a short sale. Homeowners frequently favor this option over a public foreclosure auction because it allows them to maintain greater influence over the sale.

Additionally, the financial fallout is usually less severe: while a foreclosure can slash a credit score by 100 to 160 points, a short sale typically triggers a milder reduction of 50 to 150 points, which fluctuates based on the borrower’s prior payment record.

And the timeline to homeownership recovery is meaningfully different, too: the waiting period to buy another house is typically 2 to 4 years after a short sale, compared to 3 to 7 years after a foreclosure.

For Texas owners comparing foreclosure vs short sale, written lender terms matter far more than verbal assurances. Kelly Legal Group notes that because the short-sale process averages 90 to 120 days, understanding the differences in control, credit impact, mortgage waiting periods, and deficiency language before closing isn’t optional; it’s the whole ballgame.

That legal reality is especially relevant for Texas non-judicial foreclosures, which can move very quickly. Because many states allow deficiency judgments for years after foreclosure, homeowners face significant financial exposure if the lender doesn’t clearly waive the remaining balance in writing.

A professional legal review helps owners confirm whether a short sale actually closes the financial risk they think it does, rather than leaving a liability that surfaces years later.

Loan Modification and Forbearance When the Home Is Still Affordable Long Term

A loan modification permanently changes the mortgage terms to make monthly payments more manageable, while a forbearance agreement temporarily pauses or reduces payments to give the borrower breathing room. These methods are best suited for owners experiencing a temporary, recoverable hardship who anticipate stable future income.

With the South leading the nation in foreclosure surges, these retention options aim to keep the owner housed rather than forcing a sale-based exit. If you genuinely believe your income situation will stabilize, this conversation with your servicer is worth having sooner rather than later.

Deed in Lieu When Preserving Ownership Is No Longer Realistic

A deed-in-lieu transfer occurs when the borrower voluntarily transfers title to the lender. This option is usually considered only after other retention or sale options have failed completely.

Since a foreclosure can drop a credit score by up to 160 points, a deed-in-lieu might offer a cleaner resolution in some cases, but homeowners must secure written confirmation detailing exactly how any remaining debt will be treated to avoid future lawsuits or surprise tax liabilities.

When Waiting Too Long Removes the Best Options

Texas Timelines Move Fast

Texas relies on a non-judicial foreclosure process, meaning lenders don’t need a lengthy court battle to reclaim a property. According to Kelly Legal Group, the average foreclosure timeline for Texas properties was roughly 135 days in 2025.

Compare that to the national average of 815 days to complete a foreclosure in the second quarter of 2024, and you start to see just how fast the Texas system can move. A homeowner who assumes they have years to figure out a solution may find themselves blindsided by an auction date they didn’t see coming.

The Warning Signs That Usually Mean Choices Are Shrinking

Repeated missed payments, an official notice of default, or a recorded notice of trustee sale all signal an accelerating process, and each one narrows the available options. If a property also requires significant deferred maintenance, its marketability drops immediately, which eats into both time and equity.

By the time a short sale process begins (averaging 90 to 120 days, though it can stretch close to a full year), an owner who waited too long may simply run out of runway before the auction date arrives.

Sound familiar? You’d be surprised how many homeowners in strong equity positions still end up at the auction step simply because they hesitated.

Why Agents and Investors Should Pay Attention Too

Real estate agents preparing for a distressed home sale in the Dallas market are likely to encounter more salvageable listings in the months ahead. Investors will see an uptick in pre-foreclosure leads, but they should keep in mind that not all of these properties will offer deep discounts.

Because substantial equity still exists in many of these homes, owners who gained 50% equity over the last five years are often positioned to demand fair market pricing rather than accept low-ball offers. The distress is real; the desperation isn’t always.

A Practical Next Step for Homeowners in Trouble

Got a notice of default? Call your servicer first and ask for two numbers in writing, the payoff and the reinstatement amount. Those figures price every decision that follows.

Then find out what the house would sell for today. Ask a local agent for a net sheet that itemizes each line, commission, taxes, repairs, liens, and the missed payments you’d owe at closing. Texas led the country in foreclosure starts early in 2026, and the sellers who came out with cash were the ones working from real numbers instead of guesses.

Call the lender’s loss mitigation department this week too. Most owners put that call off for months, and it costs them exits they still had. A HUD-approved housing counselor is free and gives you advice with no stake in the outcome.

One more thing. If your exit runs through a short sale, a deficiency waiver, or a deed in lieu, put a lawyer and a tax professional on the paperwork before you sign, because forgiven debt can surface later as a lawsuit or a tax bill. The national foreclosure average is 815 days. Texas gives you about four months.

Answers to Common Questions About Foreclosure Alternatives in Texas

Can I stop an auction that’s already scheduled?

Sometimes, and the tools shrink as the date closes in. Reinstating the loan (paying the arrears and fees in full) stops it, and so does a completed modification agreement, a lender-approved postponement, or the court-ordered stay from a bankruptcy filing. The week before the sale is late. Call for help anyway, because we’ve seen postings withdrawn five days out.

How much does each exit hurt my credit?

A completed foreclosure typically costs 100 to 160 points and stays on your report for seven years. Short sales and deeds in lieu usually land softer, near 50 to 150 points depending on the payment history that came before. The missed payments themselves do their own damage, which is one more argument for moving early.

Do I owe income tax if my lender forgives part of the debt?

Possibly. Forgiven mortgage debt can arrive as a 1099-C, and the IRS may count it as income, though exclusions cover some insolvent borrowers and some qualified principal residence debt. Put a CPA on this question before you sign. We’re attorneys, and even we route this question to a tax professional before a client signs.

The Best Option Is Usually the One Chosen Early

Rising foreclosure filings across North Texas represent a serious economic reality, but they don’t automatically spell financial ruin. Because many local owners still retain significant property value, the 50% equity growth seen over the past five years provides a critical safety net that the 2008 era never offered.

The most severe outcomes occur when homeowners freeze and allow the lender to dictate the entire timeline, culminating in a public auction that wipes out options that were still very much available weeks earlier.

Timing remains the ultimate currency in real estate distress. With national foreclosure filings climbing 10% in 2023 to 357,062 properties, ignoring the warning signs is a costly gamble. Homeowners should speak immediately with a trusted real estate agent, a HUD-approved housing counselor, or a qualified real estate attorney before a public auction date is set. The options narrow with every week that passes.

{kind=link}

{kind=link}