More and more people are choosing to rent, economists are finding, but Apartment List found in a recent study that one particular — and somewhat surprising — segment of the rental market is booming: high-income renters.

The report deems those with six-figure incomes as high-income renters, and a growing number in this income bracket are choosing to rent their homes instead of buying. On a national basis, almost two million (or 48 percent of) high-income households became renters between 2007 and 2017.

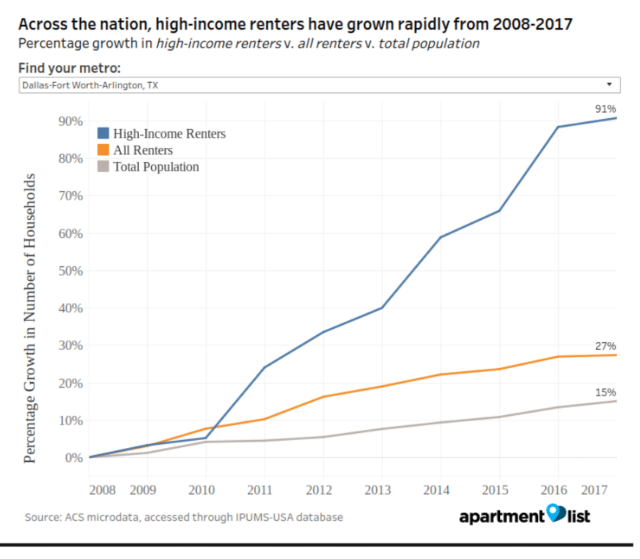

“In Dallas specifically, high-income renters grew 91 percent from 2008-2017,” said Apartment List research associate Rob Warnock.

Why? At least in Dallas, it may be the sheer volume of luxury apartments available.

At a conference at the Federal Reserve Bank of Dallas last year, RealPage chief economist Greg Willett said most of the apartment completions that cycle were luxury communities.

“Today’s typical suburban project is a mid-rise building with garage parking, rather than a low-rise development with surface parking,” he said. “Urban core projects account for a bigger share of the total building than in the past. Urban land costs drive up the rents, and high‐rise construction pushes the numbers even higher.”

In Dallas, luxury renters pay a premium of around 30 percent, and in Fort Worth, 34 percent. Both of those are lower than the national average of 38 percent. Austin and Houston have higher premium percentages at 53 percent and 45 percent, respectively.

“U.S. rent-to-income ratios are inversely correlated to apartment product class,” Willett explained. “Those who opt for Class A apartments rarely face affordability constraints — affordability gets somewhat more challenging when moving to those lower end product segments.”

“Certainly it’s always been true that those living in luxury spend lower shares of income on rent,” he added.

The fact that even luxury apartments are cheaper in Dallas than many other areas of the country, may also explain why people are choosing to rent than buy.

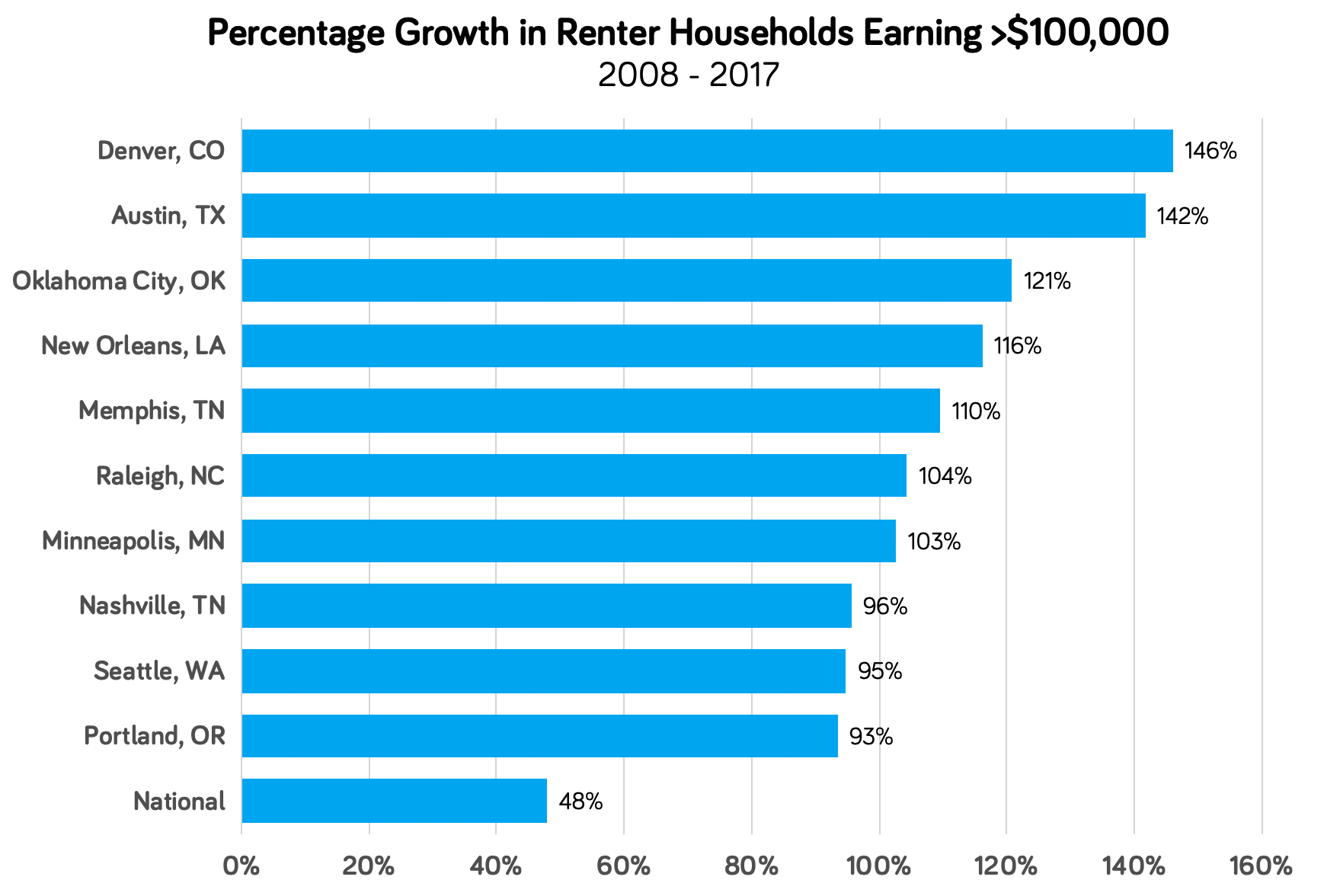

“The rise of high-income renters has been most dramatic in mid-size, growing metropolitan areas, particularly Denver (146 percent growth), Austin (142 percent), and Oklahoma City (121 percent),” the report said. Growth is slower in more expensive markets like New York and Los Angeles.

While the total population grew by six percent in the 10 years the study focuses on, incomes grew by seven percent. Denver and Austin have the highest numbers of high-income renter growth.

“These metros housed nearly 2.5 times more six-figure renter households in 2017 than they did in 2008,” the report said.

On a national level, Apartment List attributes the growth in this rental segment to several things, including an increased supply of rental options.

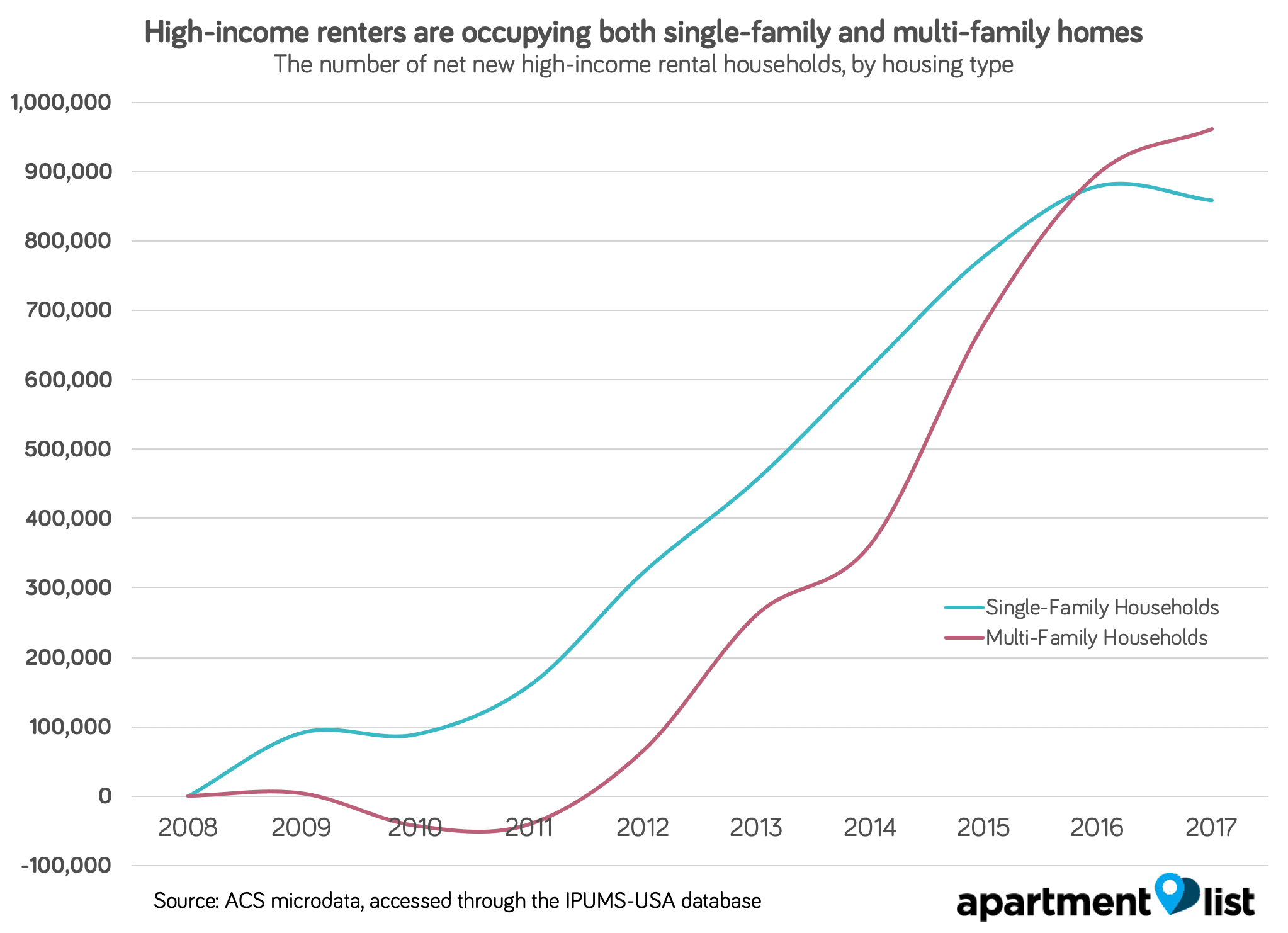

“Since the Great Recession, new supply in the marketplace has provided high-earners with abundant rental options,” the report said. “An initial wave of single-family vacancies catered to those who value the comfort of suburbia, whereas a subsequent wave of multi-family construction catered to those who value centrality and urban living.”

Prior to the recession, the U.S. was in the middle of a construction boom. But when the recession hit, suddenly new sales declined and foreclosures rose, glutting the market with plenty of investor-friendly single family homes that could be snagged and converted into rental properties, to the tune of an additional 4 million single-family rentals during that time.

“This new inventory enabled more high-income households to enjoy the extra space of single-family homes without needing to buy,” the report explained.

But in 2011, multi-family housing came back with a vengeance, bringing rental units to urban areas where density was key.

In the first three years of the recession, high-income renter households largely left multi-family homes because the vacant single-family homes were so plentiful. But as new multi-family stock began to come back in 2011, they moved back so quickly that they overtook single-family rentals by 2016.

“By 2017, there were a total of 1.8 million new high-income renter households – 960,000 occupying multi-family and 860,000 occupying single-family,” the report said.

Also by 2017, in many areas housing inventory was (and is) much lower than the six months generally agreed to be the sign of a balanced market. This lack of availability has made homeownership more expensive. Combined with more stringent mortgage requirements, slower rising incomes, student loan debt, and other challenges, even high-income wage earners feel the hardship of attempting to become a homeowner.

“Until the economic landscape changes, renting may remain the most financially feasible option for many high-earners,” the report said.

Demand is also driven by more people moving in thanks to company relocations, as well as a shift in popularity in urban cores.

What does this mean for the future of the housing market?

“In the short-term, we expect the influx of high-earning households into multi-family rentals to continue, as multi-family construction remains strong and workers value the job opportunities and amenities of living in urban areas,” Apartment List said. “With higher incomes, these households will demand new amenities from their homes and neighborhoods.”

And when high-income earners can’t afford to buy, in the medium-term, it may result in policy changes as these earners tire of renting, and of a cycle that makes home ownership purely aspirational and less attainable.

“In the long-term, this decade’s trend may be indicative of changing norms around how we pay for our housing,” the report concluded. “If today’s high-earning families increasingly value the centrality of living in cities or the flexibility of renting instead of owning, the traditional paradigm of homeownership as a paramount metric for financial success may begin to evolve.”

To see the entire report, click here.

{kind=link}