- The Short Version on Dallas Affordability

- What Zero State Income Tax Actually Means

- The Hidden Impact of Texas Property Taxes

- Rising Insurance Premiums in 2026

- Housing Costs Compared With Coastal Markets

- Utilities, Groceries, and Daily Living Expenses

- Comparing Dallas to Los Angeles

- Comparing Dallas to New York City

- Comparing Dallas to Chicago

- Comparing Dallas to Denver

- Who Benefits Most From Moving to Dallas

- The Final Verdict on Relocation Costs

Everyone assumes Texas is cheaper. It shapes relocation conversations, “leaving California” headlines, and every TikTok about Texas freedom. But the reality is more layered, especially after two years of shifting home prices, higher insurance premiums, and bigger property-tax exemptions.

Dallas is generally more affordable than Los Angeles, New York City, San Francisco, Boston, and Seattle. But the gap is not as wide as many newcomers expect. For some buyers, the savings shrink quickly once property taxes and insurance are added to the monthly payment.

Here is what the numbers actually look like in 2026.

The Short Version on Dallas Affordability

Dallas’s overall cost of living is roughly in line with the national average. That sounds modest until you compare it with the cities people are usually leaving. Dallas still remains meaningfully more affordable than most major coastal markets.

The four numbers that really move the relocation math are state income tax, property tax, insurance, and housing prices. Get those four right and you can usually tell whether the move actually pencils out.

What Zero State Income Tax Actually Means

This is the part that does live up to the hype. Texas has no state income tax. There is no progressive bracket, no flat income-tax rate, and no surcharge on high earners because the Texas Constitution prohibits a tax on individual net income.

For someone moving from California, the difference can be substantial. Using current California tax structures and including the 2026 SDI withholding, the rough savings look like this:

- At $100K income: about $5,000 to $7,000 per year versus California

- At $150K income: about $10,000 to $13,000 per year

- At $250K income: about $22,000 to $25,000 per year

- At $500K income: roughly $50,000+ per year

California also has something many people miss: State Disability Insurance. In 2026, the SDI rate is 1.3%, and there is no taxable wage ceiling. That means a $200K California earner pays about $2,600 in SDI alone, on top of state income tax. Texas has no equivalent.

The New York comparison can be just as dramatic. NYC residents pay city income tax on top of New York State income tax, and a $200K taxable income can produce roughly $19,000 in combined state and city income tax before federal taxes.

Illinois is closer to a wash, but not completely. Illinois uses a flat 4.95% income-tax rate, so someone earning $150K still gives up roughly $7,000+ in state income tax before exemptions.

This is the foundation of every claim that Texas is more affordable. It is true, but it leaves out several major costs.

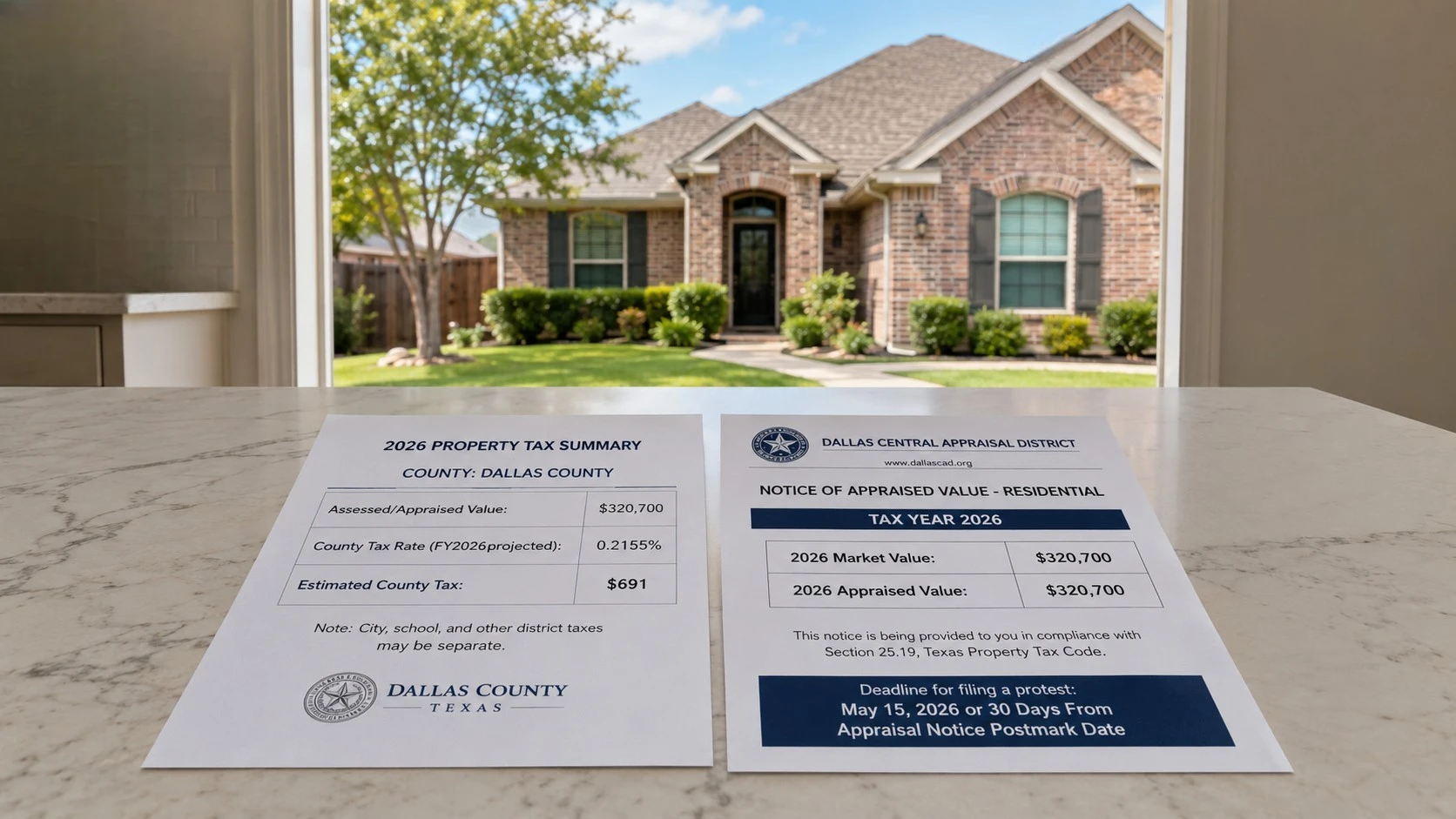

The Hidden Impact of Texas Property Taxes

Texas funds local government heavily through property taxes, and the rates are high. In many DFW cities, buyers should expect an effective property-tax burden somewhere around the high-1% to low-2% range, depending on the city, school district, exemptions, and the home’s assessed value.

In practical terms, the math can look like this:

- A $500,000 home in Plano: roughly $9,000 to $11,000 per year in property tax

- A $750,000 home in Frisco: roughly $13,500 to $16,500 per year

- A $1,000,000 home in Southlake: roughly $18,000 to $22,000 per year, sometimes more depending on exemptions and tax rates

Now compare that with California. Proposition 13 limits the general property-tax levy to 1% of assessed value, though voter-approved local assessments can push the total above that. For long-term California homeowners, the tax bill may be far below current market value because assessed value is capped. That is why a person selling a long-held California home and buying a newer Texas home can be surprised by the property-tax reset.

Recent Texas changes help, but they do not erase the issue. SB 4 raised the school district homestead exemption from $100,000 to $140,000, and voters approved that increase through Proposition 13. Homeowners who are 65 or older, or disabled, now receive an additional $60,000 school district exemption, bringing the school exemption total to $200,000 for those homeowners.

Texas also has a 10% annual cap on increases to the appraised value of a qualified residence homestead. That cap helps long-term owners, but it does not prevent taxes from feeling expensive when someone buys into the market at today’s prices.

One practical point matters: homeowners generally need to apply for exemptions with the county appraisal district, and the usual deadline is before May 1. Missing or delaying that filing can mean paying more than necessary for a year.

Rising Insurance Premiums in 2026

Nobody talked about this much a few years ago, but Texas homeowners insurance is now one of the biggest affordability issues in the state. Dallas-Fort Worth has one of the highest insurance burdens in Texas, behind or alongside Amarillo depending on the measure.

The numbers are not small:

- The average Texas home insurance premium in 2026 is about $4,085 per year

- The national average is about $2,543 per year

- Dallas-area quotes vary widely, but many buyers should budget roughly $3,500 to $5,000+ per year, depending on the home, roof age, deductible, carrier, coverage level, and ZIP code.

The drivers are severe weather, hail, wind claims, roof losses, and rising rebuilding costs. DFW sits in a major hail-risk region, and roof claims are a huge part of the insurance story. Some older homes can be harder or more expensive to insure, especially if the roof is aging or the carrier sees repeated storm risk.

Auto insurance follows a similar pattern. DFW drivers deal with heavy traffic, hail exposure, uninsured motorists, and vehicle-theft risk in certain ZIP codes. For many households, the combined home and auto insurance bill can eat into the income-tax savings faster than expected.

For a household budget, that means adding roughly $2,000 to $3,000 per year compared with a similar home in a lower-risk state. The income-tax savings often absorb it, but the margin is not as clean as the headline sounds.

Housing Costs Compared With Coastal Markets

The “Dallas is cheap” narrative still leans on old prices. The 2026 market is different.

In Dallas, recent market data shows:

- The median sold price is about $408,000

- The median listing price is about $435,000

- The median rent is about $1,665 per month

- The average one-bedroom apartment rent is about $1,400 per month, depending on source and neighborhood

The suburbs can be much higher. Collin County’s median listing price is around $500,000, Frisco is around $700,000, Plano is around $538,000, and Celina is around $585,000.

Compare that with other markets:

- Los Angeles County median listing price is about $950,000

- New York City average one-bedroom rent is about $4,100 per month

- Chicago median listing price is about $355,000

- Denver median listing price is about $541,000

Dallas is genuinely cheaper than Los Angeles, New York City, San Francisco, and Denver on most housing comparisons. Chicago is the tricky one. Chicago can still be cheaper for buyers, depending on the neighborhood, although property taxes and state income tax change the full picture.

For renters, Dallas is much easier to defend. Renters get most of the Dallas affordability advantage without taking on property tax, roof risk, or homeowners insurance. A renter moving from New York or Los Angeles to Dallas can see the savings immediately in the monthly budget.

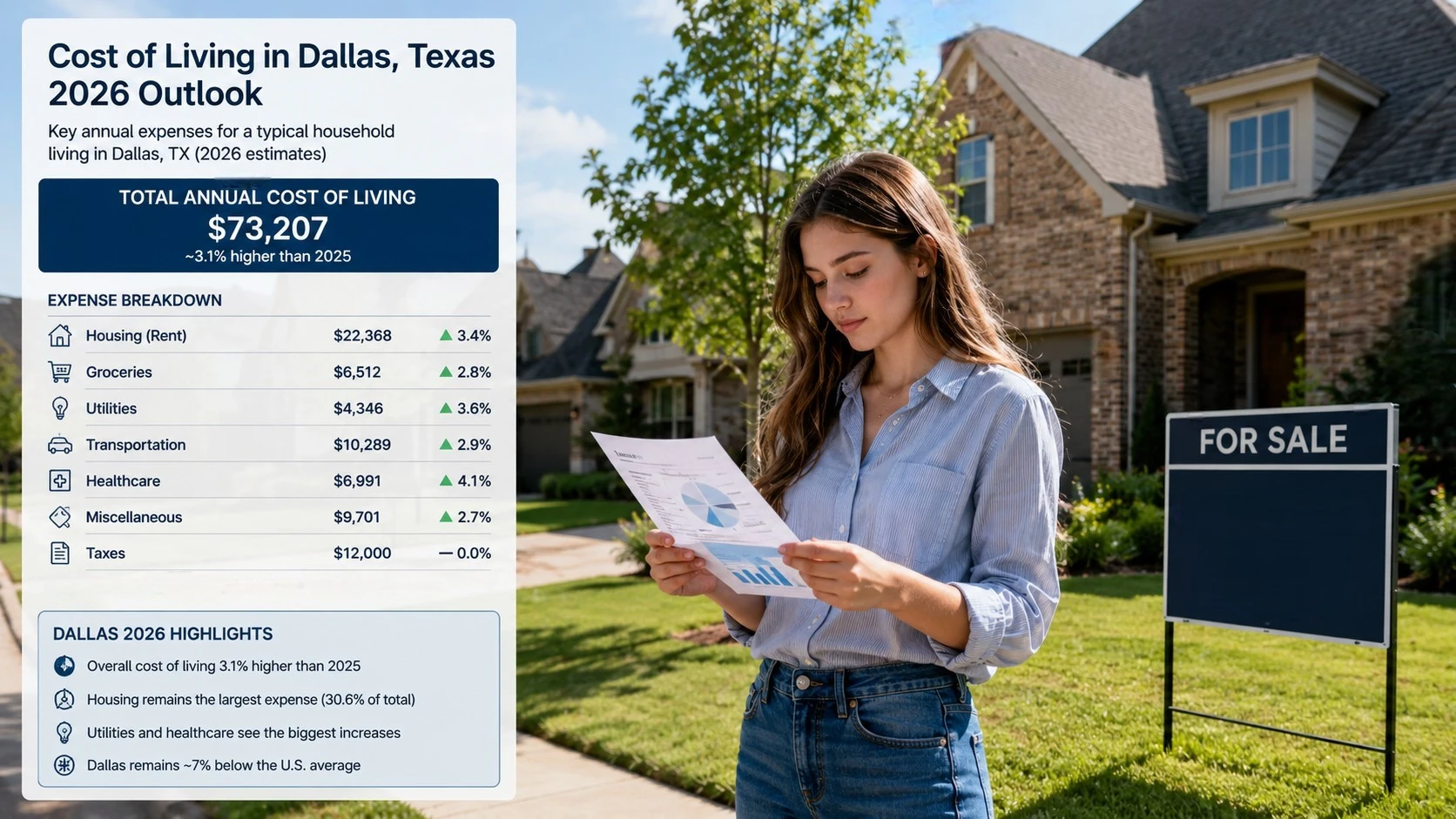

Utilities, Groceries, and Daily Living Expenses

The smaller categories matter too. Dallas is not expensive across the board, but it is not low-cost in every category.

Here is where Dallas lands relative to the national average:

- Housing: 8% below national average

- Utilities: 16% above national average

- Groceries: 1% below national average

- Healthcare: 4% above national average

- Clothing: 6% above national average

- Entertainment and personal services: 6% above national average

- Transportation: below the national average in this dataset, though car dependency still matters

The utility number deserves attention. Texas summers are long, hot, and expensive. Air conditioning can run hard from June through September, and many households see summer electric bills jump sharply.. Texas does have a deregulated electricity market, so you can shop providers. Choosing the wrong plan can cost hundreds of dollars a year. Choosing the right one can soften the summer-bill shock.

Sales tax is also part of the equation. Dallas has an 8.25% combined sales tax rate in 2026. That is not unusual for a big U.S. city, but it still matters because Texas relies more heavily on consumption taxes and property taxes instead of state income tax.

Comparing Dallas to Los Angeles

For a single filer earning $150K and buying around a $500K home, Dallas usually wins, but not by as much as people expect.

| Category | Los Angeles | Dallas |

|---|---|---|

| State income tax | High, based on California brackets | $0 |

| SDI charge | 1.3% of wages, no wage ceiling | $0 |

| Property tax | Often lower for long-term owners under Prop 13 | Often higher as a percentage of value |

| Home insurance | Varies, but often lower than North Texas for standard risk | Often higher because of hail and storm risk |

| Auto insurance | Expensive | Also expensive in many ZIP codes |

| Bottom line | Baseline | Usually cheaper, but not automatic |

Renters moving from Los Angeles to Dallas usually save much more. A Dallas one-bedroom averages around $1,400, while Los Angeles averages around $2,180 for a one-bedroom apartment. That alone can save roughly $9,000+ per year before taxes.

Comparing Dallas to New York City

New York City to Dallas is the clearest cost drop for many households. NYC rent, city income tax, state income tax, and daily living costs are all heavy.

A New York renter moving to Dallas can often cut rent by thousands per month. But there is a lifestyle trade-off. New York offers walkability and transit. Dallas is far more car-dependent, so newcomers may add a car payment, insurance, gas, tolls, parking, and maintenance.

Even with that added car cost, Dallas usually comes out ahead financially for most NYC movers. The bigger question is whether the lifestyle change works.

Comparing Dallas to Chicago

This is the comparison that surprises people. Chicago has lower median listing prices than Dallas, stronger public transit, and many neighborhoods where buyers can get more home for less money.

But Illinois has a 4.95% flat income tax, and property taxes in the Chicago area can be high. The savings from moving to Dallas are smaller here than they are for someone leaving California or New York. For some households, Chicago may actually be cheaper on pure housing cost. Dallas wins more often on job growth, taxes, newer housing stock, and long-term metro growth.

Comparing Dallas to Denver

Denver is a more straightforward comparison. Colorado has a flat 4.4% income tax, and Denver home prices remain higher than Dallas in many comparable areas. A $150K earner can save about $6,600 per year in Colorado state income tax alone by moving to Texas, before property tax and insurance differences.

Insurance is not a clean win either way because both regions deal with hail. But for many buyers, Dallas still comes out cheaper because the housing entry point is lower.

Who Benefits Most From Moving to Dallas

Here is who tends to save the most:

Big winners:

- Renters at almost any income level, especially those leaving coastal markets

- High earners buying homes under about $600K

- Remote workers keeping coastal salaries

- Business owners with pass-through income

- Retirees with modest taxable income, since Texas does not tax Social Security or retirement income at the state level

Moderate beneficiaries:

- Middle-income families buying homes between $400K and $700K

- People moving from California, New York, or Illinois for a similar salary

- Buyers who file their homestead exemption on time

- Households that shop insurance and electricity plans carefully

Likely break-even cases:

- Buyers purchasing homes above $800K

- Long-term California homeowners protected by Prop 13 who sell and rebuy in Texas

- People moving from Chicago or other relatively affordable Midwest metros

- Households with multiple cars and high insurance costs

Potentially higher-cost cases:

- Retirees with expensive paid-off California homes who buy expensive Texas homes

- Buyers who forget to file the homestead exemption

- Buyers purchasing older homes with roof, foundation, or insurance issues

- Luxury buyers who assume Texas property taxes will be low because the state has no income tax

The Final Verdict on Relocation Costs

Dallas is cheaper than the coastal markets people are usually leaving, but the savings are not automatic. The income-tax advantage is the biggest reason the math works. Property tax and insurance are the biggest offsets.

A simple way to estimate it:

- Take your projected income.

- Subtract what you would pay in your current state income tax.

- Add back the higher Texas property-tax burden.

- Add the likely insurance difference.

- Then compare housing costs honestly, not emotionally.

For most households earning above $100,000 and buying under $600,000 to $700,000, Dallas still pencils out. For renters, the move is usually strongly favorable. For buyers above $1 million, the math gets much closer than the headlines suggest.

The good news is that none of this requires guessing. County appraisal districts publish tax information. Insurance quotes are free. Electricity plans can be compared before move-in. Take-home-pay calculators are easy to run. The people who get burned are usually the ones who trust the “Texas is cheap” narrative instead of doing the math.

Once the numbers work on paper, the next variable is execution. A move to Dallas is not just a truck and a closing date. It can involve HOA rules, elevator reservations, gated-community access, storage timing, utility setup, and a few days of overlap between homes. Hiring a Dallas moving company that understands both interstate relocations and local DFW moves can make that transition much less stressful.

Texas is probably cheaper than where you came from. But the margin is smaller than the internet makes it sound, and the savings only happen when the numbers are handled carefully.

{kind=link}