Property renovation projects can be profitable, but they also come with real risk. Investors buy older properties to renovate and sell for a profit. But from day one, the property is exposed to threats like damage, theft, and delays in construction work.

When materials, labor, and time are on the line, the right insurance matters. Builder’s risk insurance helps protect a property while renovation work is underway. Evaluating your policy options helps you avoid major out-of-pocket costs and keep the project on track from start to finish.

The Basics of Builder’s Risk Insurance

Unlike a standard homeowners policy, builder’s risk insurance focuses specifically on the building during the active renovation phase. Many professionals depend on organized protection strategies, including real estate investors insurance, to safeguard their properties from unexpected financial losses during purchase, renovation, and resale.

This coverage typically pays for structural damage and materials stored on the job site. It may also cover renovation equipment kept at the location. Understanding these basics helps you find a policy that actually fits the size and timeline of your specific project.

When to Buy and What It Costs

It is crucial to lock in your builder’s risk policy before anyone swings a hammer. Most insurance carriers will not write a policy if the renovation is already more than thirty percent complete.

As for the cost, expect to pay anywhere from one to four percent of your total construction budget. The exact price depends on the location of the property, the scope of the work, and the type of materials you are using.

What Does Builder’s Risk Insurance Cover

Builder’s risk policies vary between providers. Because of this, reviewing the essential coverage elements is important before choosing a plan. You will want to look for a few key areas of protection.

Structural protection helps cover the property during renovation from damage caused by unexpected events like fires or severe storms. Material coverage protects building supplies stored on the property before they are actually installed. Temporary structure protection covers things like scaffolding and construction trailers while work is in progress.

Debris removal assistance can help pay for cleanup costs after property damage occurs. Project delay protection may compensate you for lost income or extra loan interest if an insured event pushes back your timeline.

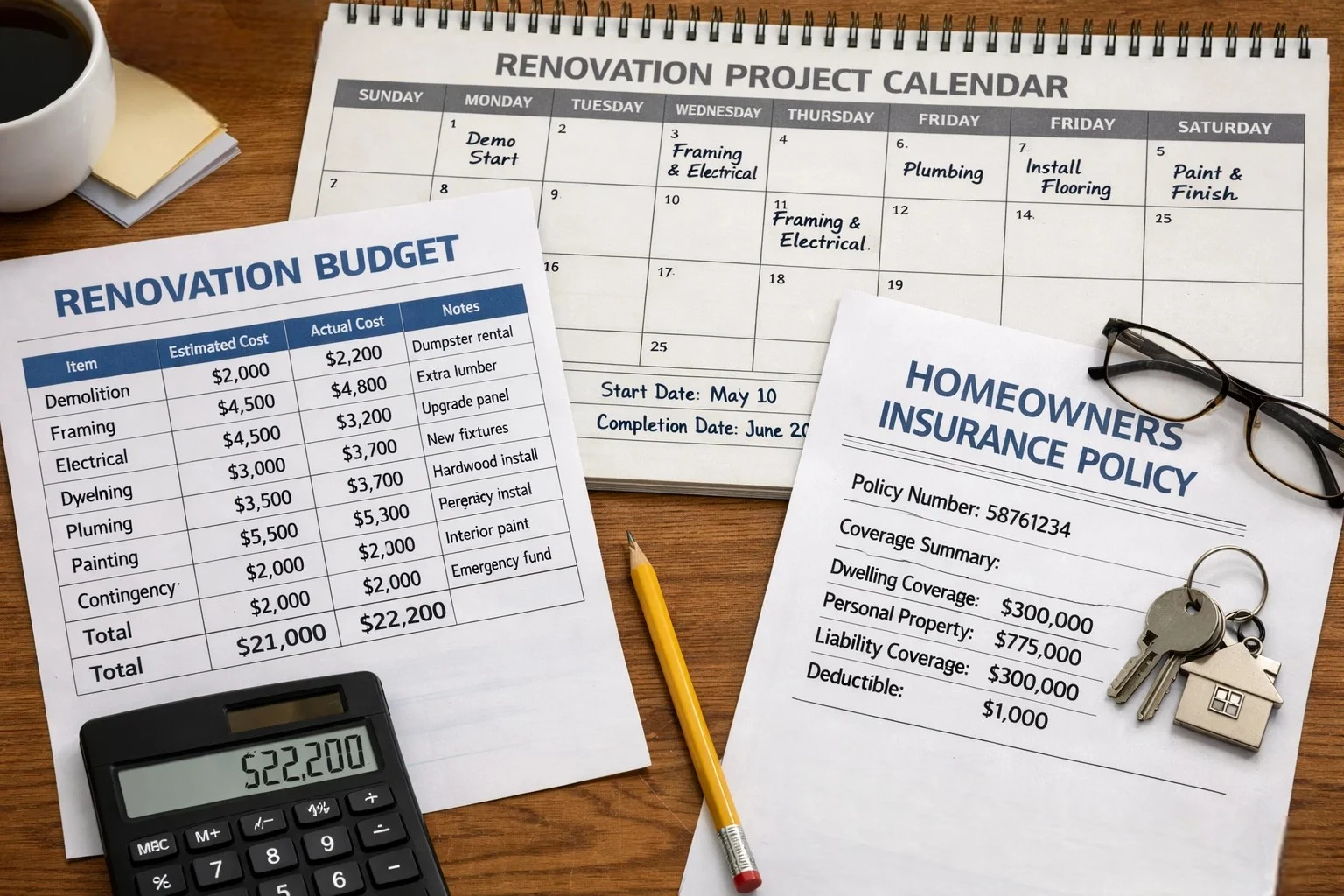

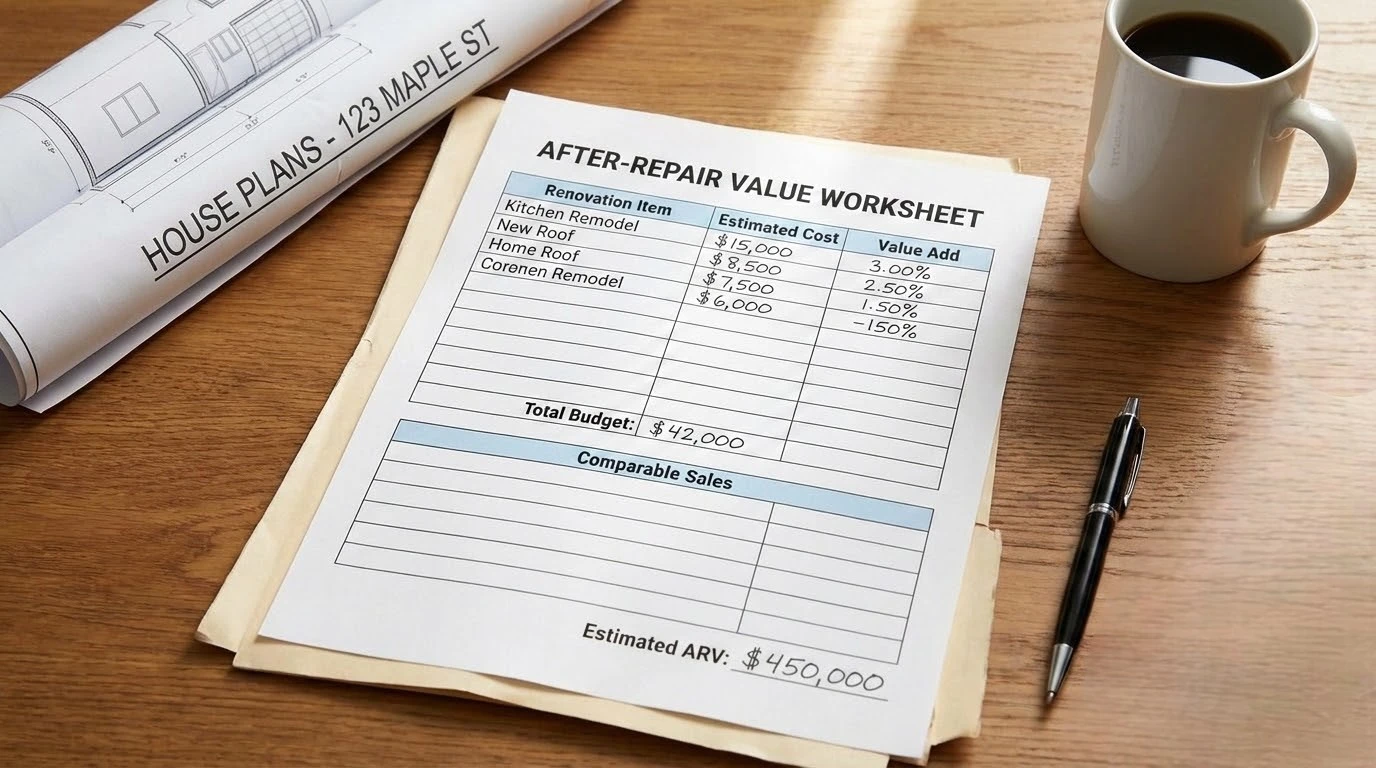

Project Value and Coverage Limits

Evaluating the true value of a renovation project helps determine the right coverage level. Investors should consider the full projected value after renovation, or ARV, rather than just the purchase price. Materials, labor costs, and improvement expenses all add to the property’s total risk exposure.

Selecting coverage based on an accurate value keeps your project fully protected during every stage of construction. A careful estimate also helps prevent underinsurance. This is vital because coming up short could leave you paying out of pocket after unexpected damage.

Policy Details To Review

Beyond basic coverage, several policy factors influence how effective a builder’s risk policy will be during renovation. You should check a few specific details before signing.

- Policy duration must match the estimated construction schedule to prevent coverage gaps

- Deductible structure affects how much cost investors pay before insurance assistance begins

- Coverage limits determine the maximum amount the insurer will provide for damages

- Exclusion details reveal which types of damage may not qualify for compensation

- Claim processing efficiency influences how quickly financial support becomes available after a loss

Common Exclusions to Watch Out For

Coverage can vary widely from one policy to another. This means you need to read the exclusions carefully. Some builder’s risk policies will not cover floods, earthquakes, normal wear and tear, or liability claims.

Employee theft and poor workmanship are also frequently excluded. This is why reading the fine print matters before work begins.

Risk Assessment

Every renovation project comes with its own set of risks depending on the condition of the building and the scope of the renovation. Investors should examine possible hazards before selecting coverage. Older structures might have hidden electrical issues, foundation weaknesses, or outdated plumbing.

Construction activity also introduces risks related to tools, equipment, and temporary exposure to bad weather. Performing a risk assessment allows investors to choose coverage that aligns with the property’s vulnerabilities and the renovation plan.

How To Compare Providers

Selecting the right insurance provider requires looking at a few practical factors that show their long-term reliability.

Financial stability indicates the company has the cash reserves to handle large claims effectively. Customer service responsiveness ensures you get help fast during urgent situations.

Claims approval reputation reflects how fair and fast the provider is when disaster actually strikes. Policy flexibility allows you to extend the timeline if renovation plans run into delays. Clear documentation helps you understand the exact terms before signing any agreement.

Balancing Cost and Coverage

Insurance cost plays a major role in your project profitability, but the cheapest policy is rarely the best choice. Instead of just looking at the monthly premium, it is smarter to weigh the actual depth and reliability of the coverage.

A stronger policy usually delivers better value because it helps protect both the physical property and your project budget. Proper insurance ensures that a stolen lumber delivery or a sudden fire does not wipe out your profit margins.

Protecting Your Investment

Successful renovation projects depend on preparation and careful financial planning. Many real estate investors rely on builder’s risk insurance to protect their financial interests while construction work moves forward. By examining coverage elements, provider reliability, and the total project value, you can make informed decisions.

A thoughtful evaluation process ensures that your renovation plans remain secure even when the unexpected happens. With the right protection in place, you can focus on getting the work done, selling the house, and turning a profit.

{kind=link}