If you’ve lost your home to foreclosure, you’ve probably heard the same advice. Rent for a few years. Rebuild your credit. Apply for an FHA loan when the waiting period ends.

That’s not wrong. But it skips the hardest part.

Nobody tells you that foreclosure makes renting hard, too. Or that how you rent during those years is going to affect whether you can actually buy again when the time comes.

Foreclosure Doesn’t Just Hurt Your Mortgage Chances

So here’s what catches you off guard. A foreclosure doesn’t only matter when you apply for another mortgage. Tenant screening reports can include information from credit reports, too. And most Dallas apartment communities run tenant screening, credit checks, or both.

A lot of management companies may treat a foreclosure as a serious rental risk, especially when it appears alongside late payments, collections, or other negative credit history. Some will decline automatically. No conversation, no context, no second look.

So you go online, pick a community that looks good, pay the $15 to $50 nonrefundable application fee, sometimes more at larger communities, and get denied. You try another one. Denied again. A third. Now you’ve burned through $45 to $150, maybe more, and you still don’t have a place to live.

That’s not a credit problem. That’s an information problem.

Some Dallas communities will absolutely work with you if you have a foreclosure on your record. Others won’t. Period. The difference is knowing which ones before you apply.

Now, if your credit has already bounced back above 620 and the foreclosure is more than three years behind you, you can probably handle this search on your own. But if you’re still inside that window, or your score is somewhere in the 500s, good luck getting approved without some help.

The Part That Affects Whether You Can Buy Later

This is something you don’t think about until it’s too late.

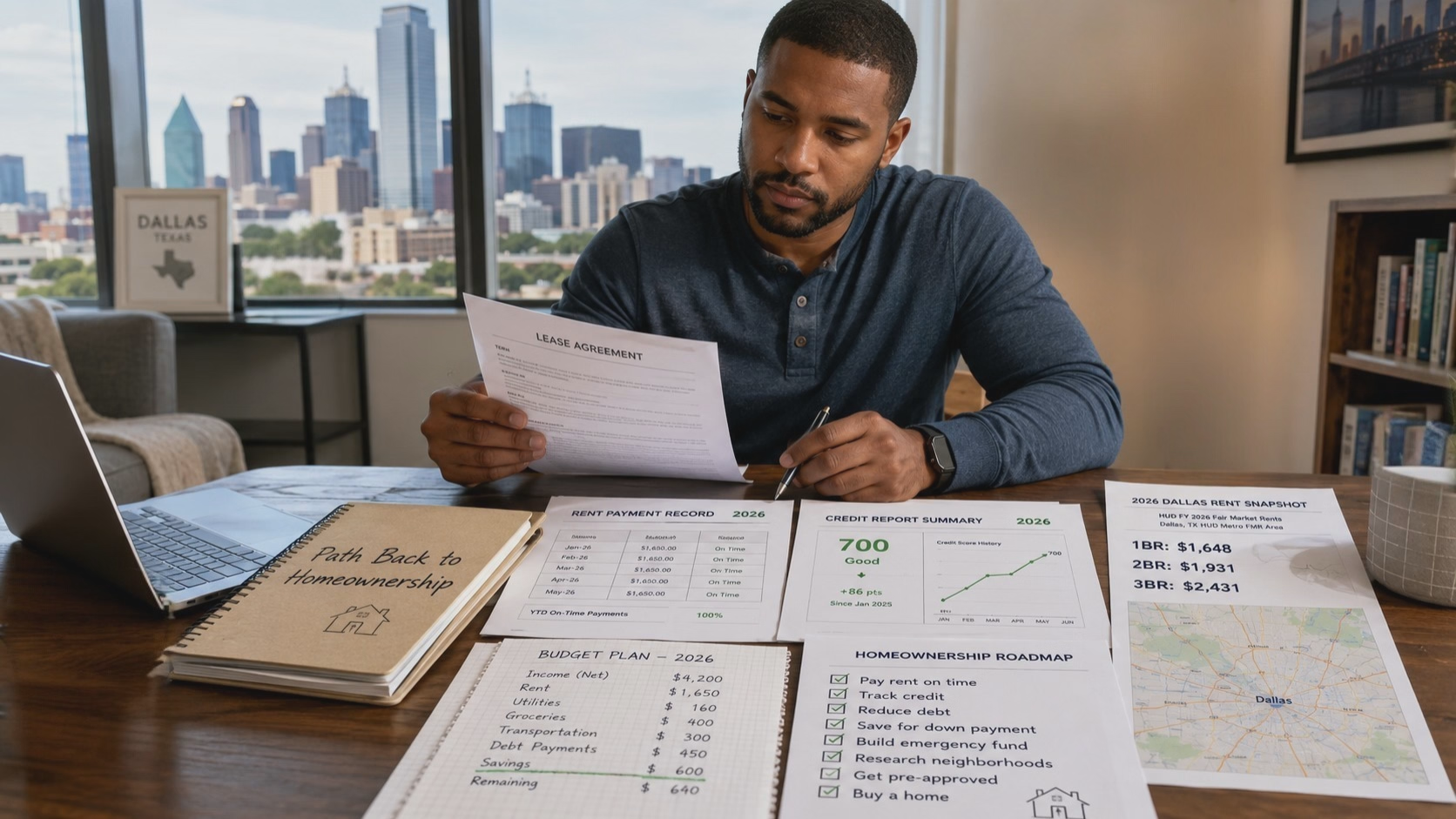

The FHA waiting period after foreclosure is generally three years. And that clock usually starts from when title transferred out of your name through the foreclosure sale or deed-in-lieu, not when you first missed a payment. After those three years, you may be able to qualify for an FHA loan with a credit score of 580 or higher and a down payment as low as 3.5%, as long as the rest of your file qualifies.

That’s a real path back to buying a home. But there’s more to it.

When a lender reviews your file, they’re not just looking at your credit score. They want to see what you did during those three years. FHA now allows positive rental payment history to be considered in certain first-time homebuyer files, and that means 12 months of on time rent payments they can actually check. A lease in your name, paid on time every month, to a landlord or management company that will confirm it in writing.

That’s the difference between a strong application and a weak one.

And here’s where a lot of you run into trouble. If you can’t get approved at a conventional apartment, you end up in a rental that won’t help you when it’s time to buy. A cash only room off Craigslist. Some month to month setup with a private landlord who doesn’t keep records. Or a sublease where your name isn’t even on the agreement.

Those arrangements keep a roof over your head. They won’t help you get a mortgage.

Think about it this way. Two people walk into a lender’s office with the same 590 credit score. One has three years of on time rent payments from a management company that picks up the phone when the lender calls. The other has a Venmo trail to a roommate. Not the same position.

What to Look for in Your Next Apartment

If you want to buy again, pick your apartment carefully. A few things matter more than the amenities list.

- A lease in your name. Not a sublease, not some handshake deal. Your name on a 12 month lease with a property management company.

- A management company that will verify your rent payments. When your future lender calls to confirm your payment history, someone needs to answer that call and put it in writing.

- A community that will actually approve you. They exist all over Dallas. Some management companies will actually look at your situation instead of just running a score. Others have programs that can help you get approved even with bad credit, as long as you have the income. If you’re not sure where to start, second chance apartment leasing in Dallas can point you in the right direction.

While you’re renting, don’t forget about your credit. Get a secured credit card and keep a small balance paid in full every month. Don’t use more than 30% of your total credit limit. And above all, no new negative marks. One late payment or new collection can set the whole timeline back.

Don’t Treat Renting Like Dead Time

The biggest mistake you can make? Treating the rental period like it’s just something to get through before the real goal starts.

It’s not. Those three years are when you prove to a lender that you can handle a mortgage. The right apartment gives you stable housing now and a payment history that backs you up when you’re ready to apply.

And if you’re in DFW and thinking about what comes next, start figuring this stuff out now. It makes everything easier.

{kind=link}