Long ago I was told that it’s more lucrative to be paid to think than to do. Turns out that piece of advice is true on many levels that intersect with homeownership.

Several years ago, the Federal Reserve Bank of New York released data that seemed to say that student loan debt was dragging down homeownership rates among younger buyers. It’s a belief that persists.

At first blush, it makes sense. If you have more debt, you have less to spend on housing because your debt-to-earnings ratio was weakened. However, new research is blowing a hole in that homily. It seems that when corrected for education, it’s not debt that’s holding back homeownership rates, it’s education itself.

You see, the New York Fed only measured those with student loan debt and those without. So while those with debt could easily be said to have been to college, those without debt included those who never attended college AND those who attended without debt.

A new research paper authored by Susan Dynarski for the Brookings Institute [available below] separated out those groups and completely changed how we should view homeownership, education, and debt. The paper shows that it’s not debt that is holding down young homeowner rates, it’s education.

Pre-recession, 35 percent of younger, college educated debt-free people bought homes. Post-recession this had dropped to 26 percent. For those without a college education, the pre-recession percentage was 23 percent, shrinking to 17 percent post-recession. Both groups dropped by a similar 26 percent, meaning regardless of recession forces, lack of a college education impairs the ability of young people to own a home.

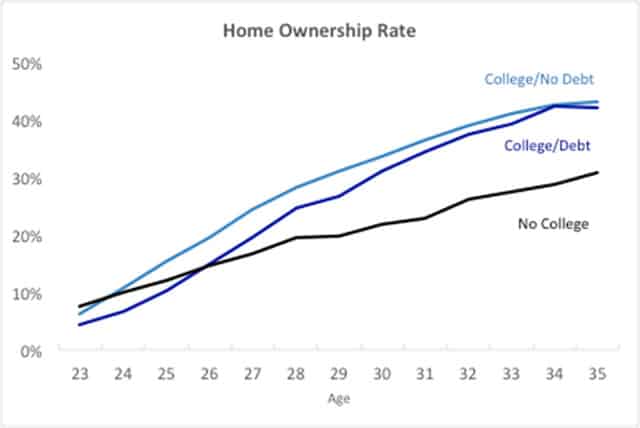

But what about college educated with and without debt? Turns out that those without debt get into homeownership sooner but by age 35, their homeownership rates are almost identical to those who started out with debt. The reason is that is takes about 10 years for the average student loan debt to be extinguished, therefore delaying their entry into housing. It’s also probable that some of those without debt got a boost from wealthier parents who similarly footed the bills for college.

The story for high school graduates is bleaker. Earning on average $25,000-$35,000 per year less, by age 35, only about 30 percent are homeowners. The picture becomes even clearer when we understand that inflation-adjusted incomes for high school graduates have been dropping since 1979. This compares to the college educated who have hit nearly 44 percent homeownership by 35 years of age.

Aside from the headline-grabbing stories of students with hundreds of thousands of dollars in student loan debt and degrees in art history, a college education, even with a reasonable amount of debt, is still the ticket to homeownership.

High School Isn’t Enough

There was a time when a high school diploma got a job that equated to a decent standard of living. Jobs where you worked with your hands in one form or another. We all know those jobs continue to vanish at an alarming rate. This leaves those heads of households with diminishing options for jobs likely making less money and impacting their housing options.

As someone who started school at age five, I can tell you that as a species, we’re not all great minds capable of (or sometimes desirous of) “thinking” work. For months I walked by a school in Dallas that had a sign posted “Every child is a genius.” No, categorically, they’re not. All brains are not Einstein.

Because we’re not all designing spaceships and curing cancer in our spare time, for society to function, there needs to be meaningful work at meaningful pay for its citizens. According to a 2014 Pew study [LINK], middle-class income was defined as ranging from $44,083 to $144,250 for a household of four. Compare that to the Economic Policy Institute that calculated that it costs between $49,114 and $106,493 for the same four-person household to live in various parts of the country. The translation is that even in the cheapest place in the country ($49,114), the lowest middle-earning family can’t survive ($44,083).

I would hazard a guess that the lowest of the middle-wage group are the non-college educated who are then much less able to purchase a home.

Putting a Bow on It

To review. Student loan debt has only a temporary effect on homeownership. Education itself is the key to increasing the odds of homeownership, but not everyone is cut out for college or “thinking” jobs. Those “do-ers” without college aptitude or education face ever decreasing job opportunities and salaries which impairs their ability to own a home (and indeed eking out a reasonable lifestyle).

The dividing line between haves and have-nots in home ownership: Education, not student debt by Joanna England

Remember: Do you have an HOA story to tell? A little high-rise history? Realtors, want to feature a listing in need of renovation or one that’s complete with flying colors? How about hosting a Candy’s Dirt Staff Meeting? Shoot Jon an email. Marriage proposals accepted (they’re legal)! [email protected]

{kind=link}