There’s been a pretty steady drumbeat from leading economists — a recession is coming. In fact, at this month’s National Association of Real Estate Editors journalism convention, all three economists on a dais one Friday found themselves agreeing on two things: a recession is coming, and real estate won’t be the impetus this time.

Frank Nothaft (Corelogic chief economist), Danielle Hale (economist with Realtor.com), George Ratiu (research director with the National Association of Realtors), and Aaron Terrazas (senior economist with Zillow) all agreed that other factors — like tariffs, rising mortgage rates, and even a correction in the stock market — will likely be the cause or causes for a recession.

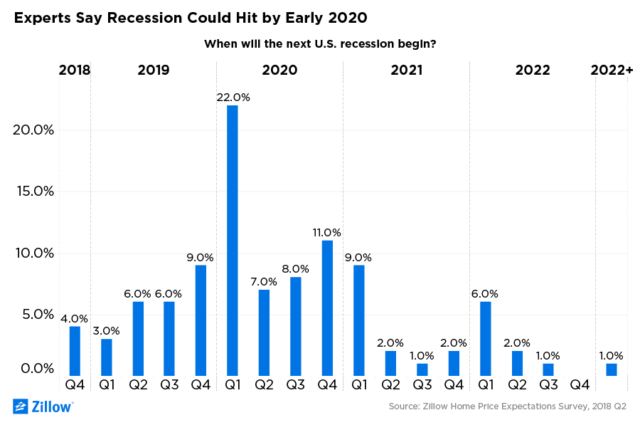

Nothaft (and most economists) said that the recession won’t happen in the next 18 months. “The odds are pretty remote for next year,” he said. “By far, most economists think it will be 2020 or 2021 or later.”

In fact, Nothaft said he thinks the current expansion will definitely continue for the next year and a half, adding that Corelogic projects a 3.3 percent growth in the economy next year, with a 16 percent probability in a recession next year.

“I feel the economy going forward still has some room to grow,” Ratiu agreed.

“The longer this economic expansion goes on the more we are asking is about when it will end,” Terrazas said, adding that he agreed with the most common projection of somewhere in 2020. “When it does come, it’s unlikely that the housing market nationwide will be the central protagonist.”

But another question looms — are we in a real estate bubble, and will the possibility of a looming recession burst that bubble?

Hale said that the current market is highly competitive — “it’s the most competitive home buying period in history.”

Supply, she said, is not keeping pace with demand, which is driving price, too.

“Inventory is at record lows and continuing to decline, down six percent in May,” she said, adding that prices are at record highs and still increasing — up eight percent in May.

But despite the fact that home prices (and mortgage rates) are increasing, it’s not as bad as it could be. Hale said that prices are the least affordable since 2008-2009, but still more affordable than most of the early 2000s and 1990s.

“Home shoppers know that it’s tough, but they’re sticking around,” she said, citing a recent Realtor.com survey that revealed that 35 percent of shoppers are anticipating a lot of competition, and 94 percent are actively employing strategies to compete.

“Nearly three-quarters of shoppers started their home search in 2017,” Hale added.

Those competitive strategies home shoppers are using, she said, include trying to put more than 20 percent down or offering more earnest money. Shoppers are also widening their search scope to include smaller homes, less expensive homes, different neighborhoods, or even economizing elsewhere to increase their monthly housing budget.

“They’re staying informed of the housing market, or they’re bringing cash to the table,” Hale said.

And for the most part, they’re staying optimistic, too — more than 70 percent of those surveyed said they expect to close on a house this year.

“Affordability isn’t kicking people out of the market, but they are making adjustments,” she said.

One growing market is the millennial market. “That homeownership rate for the under 35 crowd is up a percentage point over the past year,” Terrazas said. Zillow’s survey of millennials who are either actively looking for a home or are entertaining the idea of purchasing found that 87 percent of young adults said their ideal home is owner-occupied, and 75 percent said their ideal home was a classic detached single-family house.

When asked where they wanted to live, those millennials surveyed said their ideal home is in the suburbs, Terrazas said.

But are we in a bubble?

Terrazas said Zillow’s analysis found home values are rising at their fastest pace since 2006, and that’s partly due to supply.

“They actually picked up over the last six months of this year,” Terrazas said, adding that while the main factor is a lack of supply, “but also slightly overstated conventional metrics.”

“Homes that hit the market tend to move very fast,” he said, and recent tax cuts have provided a modest boost to the housing market.

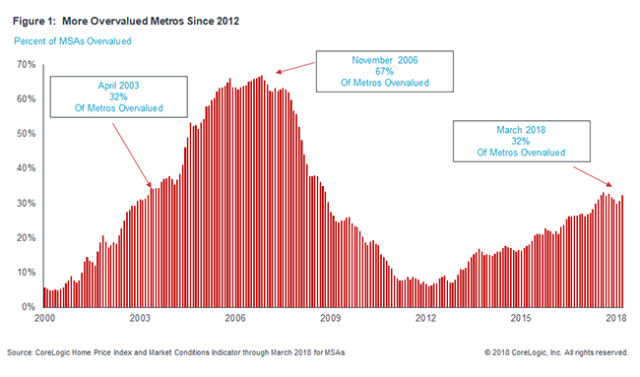

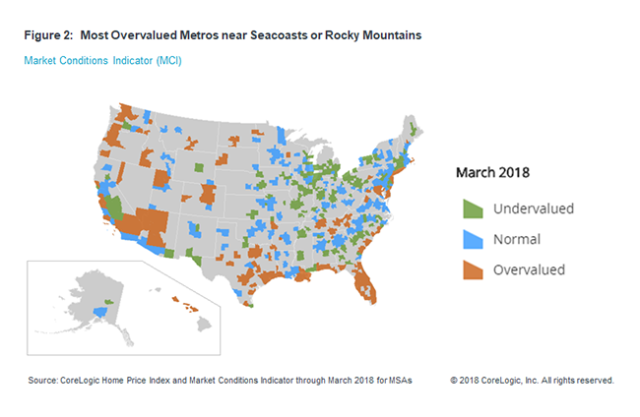

Nothaft said that Corelogic looked at 390 metro areas, and found that 32 percent were overvalued on March 2018.

“The last time it looked overheated, was in 2003 (where it was at 32 percent), and it peaked on November 2006 with 67 percent overvalued,” he said.

In other words, while we don’t necessarily have a national bubble right now, continued rapid home price growth can potentially create a situation where a new bubble could form in the next few years.

“We may very well see prices come down, and come down very sharply when recession does happen,” Nofthaft said. “If we did hit a recession, I would expect that the Fed would temporarily reduce interest rates again.”

A recent Zillow/Pulsenomics poll of economists said that the housing market will likely see a stronger price appreciation — with home values rising 5.5 percent to a median $220,800 in 2018. Last year a 3.7 percent gain was predicted.

Terrazas said that a lot of variables will go in to how hard the housing market is hit by a recession, including the severity and length of the recession, how high unemployment climbs, and where you are in the country.

“It’s not necessarily meaning that it’s all going to come crashing down,” he said.

{kind=link}