- Why Financial Coordination Matters in Real Estate Transitions

- Understanding Equity Beyond the Sale Price and Mortgage

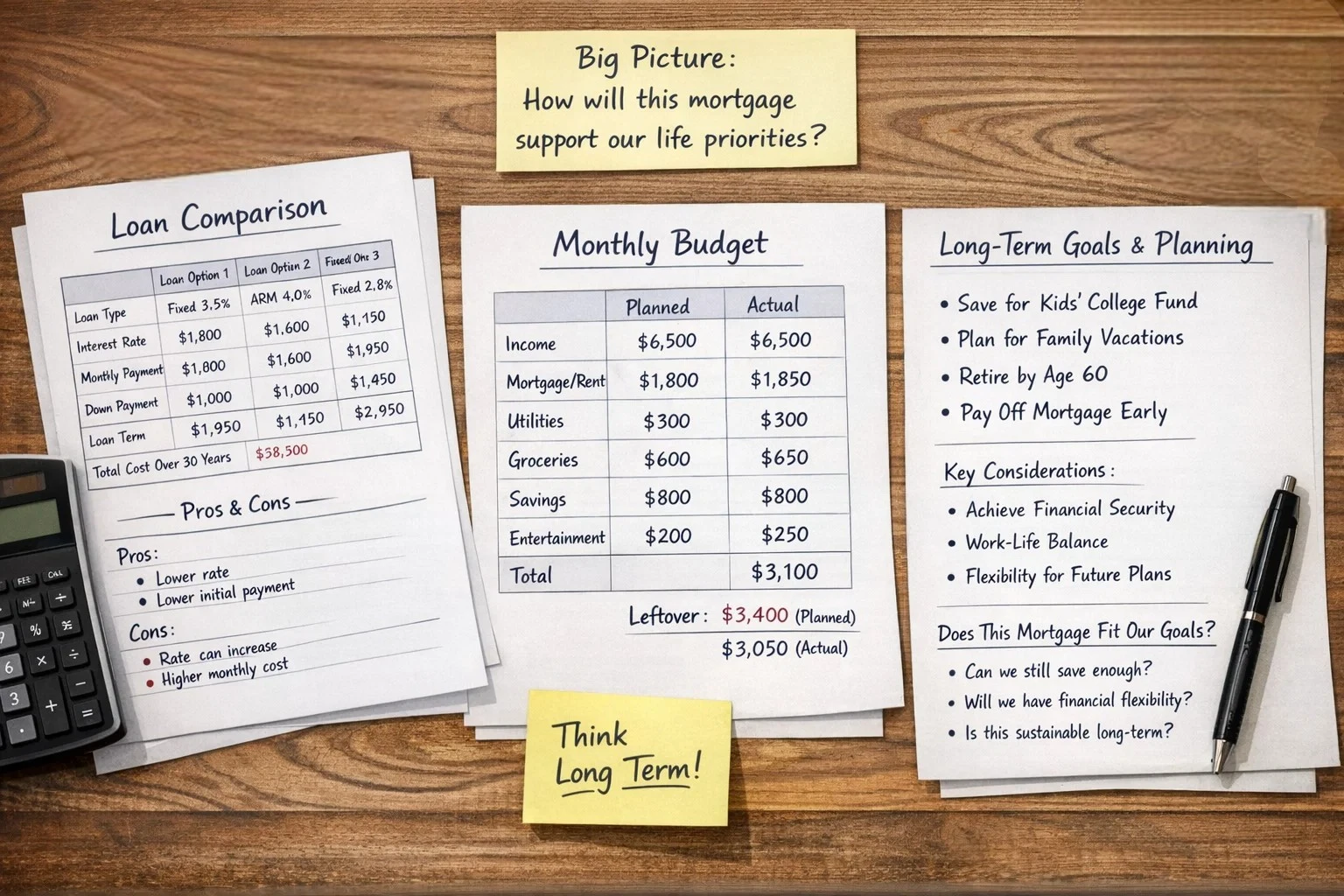

- What Bridge Financing Is and When It Matters

- Refinancing as an Alternative Strategy

- Market Timing, Interest Rates, and Appraisal Outcomes

- Why Closing Costs Are Often Underestimated

- Avoiding Common Financial Mistakes

- Aligning Financing With Long-Term Life Goals

- Reducing Stress With a Clear Plan

Buying or selling a home is usually talked about in terms of neighborhood appeal, school districts, and interior finishes. But the financial side of juggling both transactions is far more complicated than most people expect, especially when selling one home and buying another happen close together and figuring out the money becomes a major part of the move. Without careful planning, what could have been an easy move can turn into stressful negotiations and unexpected costs.

This is where looking at the big picture really matters. The timing, your access to equity, bridge financing options, refinancing strategies, and even the order of each closing can all affect how everything unfolds. Many homeowners find value in working with a mortgage agent offering the best services in the area early in the process. This isn’t just for loan approval but to figure out a solid plan that fits their overall goals. This professional perspective helps clarify how short-term choices affect long-term financial stability.

Why Financial Coordination Matters in Real Estate Transitions

Lining up your finances becomes especially important when the sale of one property has to fund the purchase of another. At first glance, it may seem straightforward. You sell house A, take the cash, and buy house B. In reality, each step involves timing, lender requirements, and closing logistics that rarely match up perfectly.

For example, the sale of a home may close later than anticipated, while the contract to buy a new home has a fixed closing date. The appraisal might come in lower than expected, and interest-rate locks may expire before the purchase closes. Each of these variables can impact your available funds or borrowing power, especially when rates are rising or markets are shifting.

Handling these moving parts without a solid plan can leave homeowners scrambling to adjust deposits, renegotiate terms, or secure short-term financing. All of this just adds stress and extra costs.

Understanding Equity Beyond the Sale Price and Mortgage

Equity is one of the most misunderstood financial concepts when moving. Many sellers assume that the difference between their home’s sale price and the remaining mortgage balance is fully available for their next purchase. What they often overlook are the transaction costs that reduce that equity.

Your true net proceeds after selling should actually account for several expenses. These includes:

- Real estate agent commissions.

- Closing costs and legal fees.

- Mortgage discharge or prepayment penalties.

- Property tax prorations.

- Transfer fees or other jurisdictional costs.

Failing to account for these deductions can lead to overestimating your purchasing power here in Calgary. A clear understanding of net proceeds ensures that you don’t count on money you won’t actually get.

What Bridge Financing Is and When It Matters

When closing dates do not line up, like when a buyer’s new home closes before the current home has sold, bridge financing can be a lifesaver. A bridge loan is essentially a short-term loan that covers the gap between the sale of one property and the purchase of another.

While bridge financing offers flexibility, it also introduces short-term interest costs and potential risk if the original property takes longer to sell than expected. If you are planning for this scenario, you need to evaluate a few things.

- Duration of coverage needed.

- Potential overlap of carrying costs.

- Fees and interest implications.

- Backup options if the sale is delayed.

The goal isn’t to assume a bridge loan is the automatic answer. It is about planning for it realistically as part of the process so homeowners are prepared for timing gaps.

Refinancing as an Alternative Strategy

In some cases, refinancing an existing mortgage before selling the property can provide access to needed funds without waiting for closing proceeds. This approach needs careful evaluation because refinancing introduces its own costs and drawbacks.

There are several factors to weigh when you are thinking about refinancing.

- Current interest rate environment.

- Remaining mortgage balance.

- Mortgage prepayment penalties.

- Long-term payment implications.

- Closing costs on the new loan.

Refinancing can make sense when it gives homeowners more stability between transactions without significantly increasing long-term debt costs. As with all financial tools, you need to weigh it against your overall financial plan.

Market Timing, Interest Rates, and Appraisal Outcomes

The timing of market shifts and interest rate movements plays a major role in making the numbers work. Even small increases in interest rates can significantly affect your purchasing power, monthly payments, and how much you can actually borrow.

Similarly, appraisals can change outcomes. A home might go under contract for more than its appraised value. This affects financing because lenders usually use the lower appraised value for loan qualification. Buyers may need to adjust their down payment, renegotiate the price, or bring extra cash to the table in these situations.

Understanding how changing interest rates and appraisal results affect affordability helps homeowners prepare realistically for the closing table.

Why Closing Costs Are Often Underestimated

Closing costs include a range of fees that both buyers and sellers must pay. Buyers face expenses like lender origination fees, title insurance, escrow fees, inspection costs, and prepaid costs. Sellers have closing costs too, including agent commissions, legal fees, and possible mortgage discharge penalties.

When two transactions occur close together, these costs overlap. Many homeowners underestimate how fast these add up, especially when they also budget for moving, new utility connections, or temporary housing.

Getting accurate estimates upfront helps keep your expectations in check and prevents you from coming up short when it matters most.

Avoiding Common Financial Mistakes

Several common mistakes tend to pop up when moves aren’t planned out well.

- Assuming gross sale price equals usable funds.

- Banking on the highest possible appraisal without a budgeting buffer.

- Making major purchases during underwriting.

- Ignoring rate lock expirations.

- Failing to model bridge financing scenarios.

- Misaligning long-term life goals with loan terms.

Identifying these pitfalls early allows homeowners to build contingency plans. Rather than reacting to issues as they come up, a good plan helps you stay ahead of them.

Aligning Financing With Long-Term Life Goals

Securing a mortgage and closing a sale are important steps, but they are not the end goal. Financing decisions should support broader life plans such as changing careers, retirement planning, growing your family, or building your investments.

Loan structures matter. Fixed-rate loans offer payment predictability but may carry higher early costs. Adjustable-rate mortgages might offer lower initial payments but come with the risk of rates going up. Amortization periods affect long-term interest costs.

A good financial plan looks beyond the immediate transaction. It involves making sure your new payment fits into your broader plans, understanding the impact of refinancing down the road, and choosing a loan structure that actually supports your long-term stability.

Reducing Stress With a Clear Plan

Moving is rarely smooth without planning. Running the numbers early on, from equity planning to rate scenarios, helps ground your real estate decisions in real numbers instead of guesswork.

When you approach buying and selling with a solid financial plan, you avoid unnecessary pressure around closing deadlines, cash flow gaps, and unforeseen costs. With thoughtful preparation, buyers and sellers can handle overlapping transactions with more confidence and less stress. Your move becomes part of a broader financial plan, not a series of last-minute decisions.

{kind=link}