Most people shopping for term insurance in India end up confused by two specific policies: return-of-premium plans and term plans without income proof.

They sound like they belong in the same conversation, but they actually serve completely different buyers.

Understanding what separates them can save a lot of time and help you avoid choosing the wrong coverage.

The Basics of Both Plan Types:

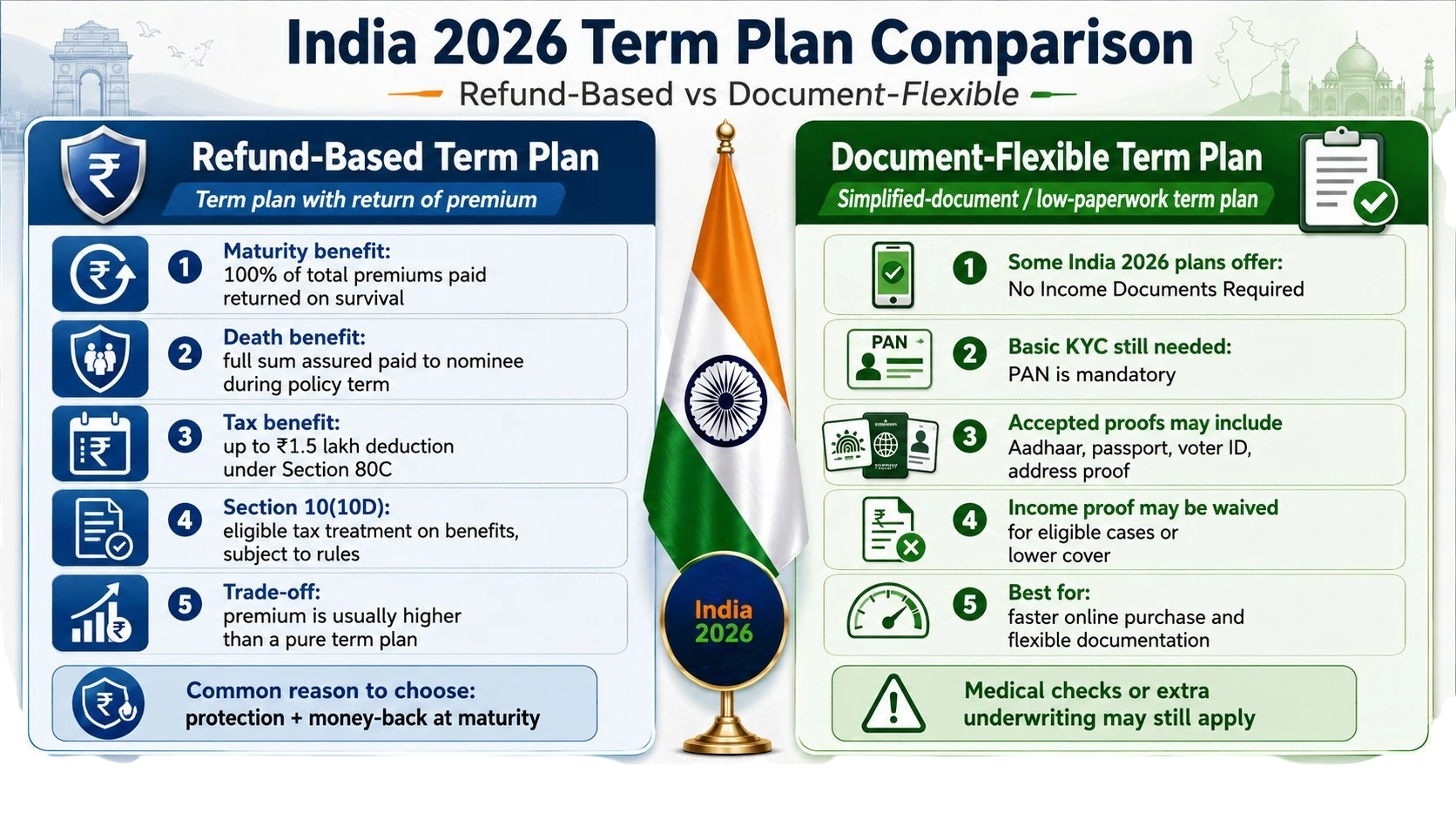

A term plan with return of premium, commonly called TROP, works like a regular term plan with one major addition: if you outlive the policy term, the insurer refunds the base premiums you paid, usually excluding taxes, rider premiums, and any extra charges, depending on the policy terms. This keeps your family protected the entire time, while also giving you money back if you survive the policy term.

A term plan without proof of income is designed for people who cannot provide standard income documents such as salary slips, Form 16, or income tax returns. This category often includes freelancers, daily wage workers, small informal business owners, and homemakers. These buyers have genuine insurance needs but fall outside the documentation requirements of standard plans.

Both are valid products built for entirely different situations.

Difference 1: What Problem Each Plan Actually Solves

A return-of-premium term plan solves an emotional problem more than a financial one. The most common complaint about regular term insurance is paying premiums for 25 or 30 years and getting nothing back if you survive. Logically, the protection was there the whole time, but many people still feel like their money was wasted.

TROP addresses that concern directly by returning those premiums at the end while keeping the family covered throughout the policy term. For someone who struggles with the idea of paying for something and receiving nothing in return, this structure makes it much easier to stay committed to the policy.

A term plan without proof of income solves a documentation problem.

Standard term plans require income proof because insurers use it to assess:

- whether the premium is affordable for the applicant

- what coverage amount is proportionate to their income

- whether the application carries any risk of over-insurance.

For salaried individuals, this is straightforward. Salary slips, Form 16, or three years of ITR usually meet these documentation requirements. But a large section of India’s working population does not fit that box.

A carpenter earning ₹40,000 a month in cash, a private tutor with irregular income, or a small trader with no formal accounts still needs life insurance. Standard plans create a documentation barrier, while a term plan without income proof may be approved with alternative financial documents such as bank statements, CA-certified statements, asset proofs, credit history, or other insurer-approved documents.

Difference 2: The Cost Structure Is Completely Different

A return-of-premium term plan costs significantly more than a basic term plan. For the same coverage amount, age, and policy length, a TROP plan can cost significantly more than a plain term plan, sometimes 40% to 100% more or even higher, depending on the insurer, age, coverage amount, and policy term. On a ₹1 crore policy for a 30-year-old with a 30-year term, the difference can be an extra ₹600 to ₹900 every month.

Over 30 years, that extra outflow adds up considerably. If that premium difference were invested in a mutual fund SIP instead, the amount built over the same period would likely exceed the total premium refund by a wide margin.

TROP makes sense for buyers who know they will not separately invest the difference and value a guaranteed return over a potential one.

A term plan without proof of income does not follow the standard premium structure in the same way. Premiums are assessed individually based on the coverage requested and the alternative documents submitted. In many cases, these plans offer lower coverage amounts because income cannot be verified with the same precision.

The premium is not necessarily higher, but the available coverage limit is often lower than what is offered to a formally employed person with similar earning capacity.

Difference 3: Who Should Actually Buy Each One

This is the most important distinction and the one most buying guides rush past.

A return-of-premium term plan suits:

- Buyers who find it difficult to pay premiums for decades without any maturity benefit

- Disciplined earners who want life coverage and a savings element combined into one product

- Anyone who has already maxed out other investment avenues and values the TROP refund as a guaranteed and predictable return

- Buyers who prefer simplicity over managing separate investments alongside a plain term plan

A term plan without income proof suits:

- Freelancers and self-employed individuals without regular documentation

- Daily wage workers or those in the informal economy

- Small business owners without formal profit and loss statements

- Homemakers who want independent coverage and can show some financial standing through bank statements

- Anyone who needs life coverage but faces difficulty with the documentation stage of standard plans

One important detail about no-income-proof policies is that the absence of standard documents does not mean skipping financial verification entirely. Insurers still need some form of financial trail to complete underwriting.

Bank statements showing regular transactions, asset declarations, and similar alternatives are typically accepted. The flexibility is in what documents qualify, not in removing the verification step altogether.

Making the Right Choice for Your Situation

If stable income and proper documents are available, the choice between a plain term plan and a TROP comes down to whether a guaranteed premium refund is worth paying 60% to 100% more every year for the same coverage.

If standard income documents are unavailable or income is earned outside the formal economy, a standard term plan may not be accessible. For many buyers, a plan without proof of income is the only route to getting covered at all.

Knowing which problem actually needs solving points you toward the right policy.

{kind=link}