Starting out as a property investor takes courage, and it takes grit to turn an idea into something that pays the bills. But there is a common reality many real estate investors face.

They are excellent at what they do, whether that’s finding deals, managing rental properties, or overseeing renovations, but are still learning how to manage the financial side of things. Small businesses rarely struggle because the owner lacks talent or passion. Instead, they struggle because the financial side isn’t built on a solid system.

Turning a side hustle into a full-time business means thinking differently. Just checking your bank balance on your phone doesn’t mean things are actually going well.

That balance doesn’t account for the tax bill due in three months, the vendor invoice due next week, a repair bill on a rental property, marketing costs for listings, or a mortgage payment on an investment property. To run a business well, the shift has to be from reactive spending to proactive management.

Mixing Personal and Business Finances

One of the most common reasons small businesses run into trouble is blurring the lines between personal and business money. When you use one account for groceries and business supplies, things get confusing fast. It becomes impossible to see the true health of your company. This lack of clarity leads to overspending and a lot of stress when April 15 rolls around. This is especially common for real estate agents, landlords, and property investors who may collect commissions, rent payments, or reimbursements in different accounts.

You need to keep your personal and business finances completely separate. Having a dedicated business checking and savings account lets business owners see exactly what the business is making. It creates a boundary that protects personal finances and ensures the company is operating on its own.

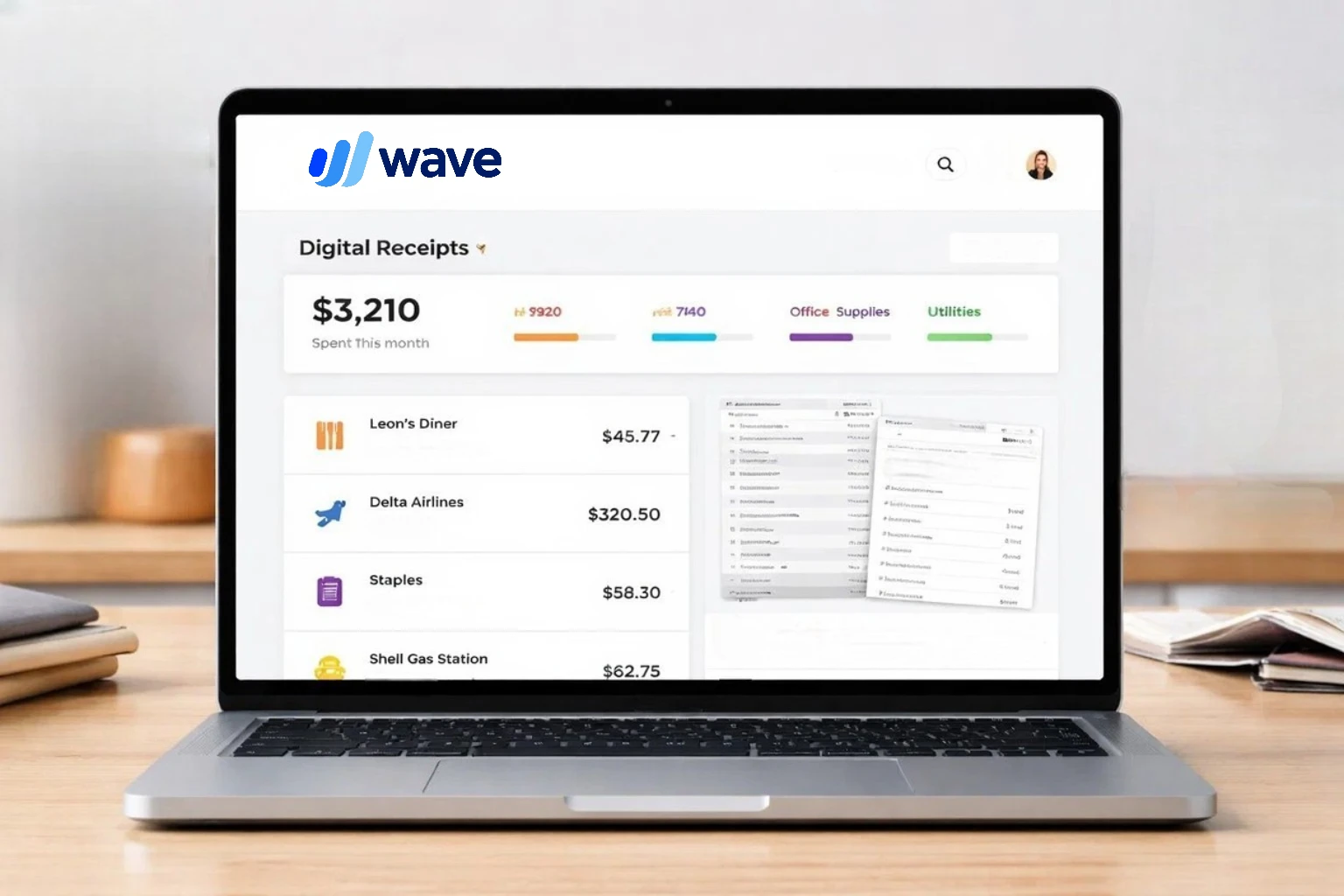

Not Using Digital Tools to Stay Organized

Many owners wait until the end of the year to gather a pile of crumpled receipts and try to make sense of everything. This often leads to missed deductions and a lot of frustration.

There’s no reason to manage everything on paper. Using the right tools to manage your business finances can change everything, especially when tracking rent payments, commissions, maintenance expenses, and closing costs. These platforms help by categorizing expenses and keeping records in one secure place.

For real estate businesses, organized records also make it easier to review property performance, agent commissions, and transaction expenses.

When you use digital systems, you get real-time data. Profit and loss can be checked at any time. Late-paying clients are easier to track without digging through an inbox. Most importantly, there’s more time to focus on growing the business instead of manually entering data.

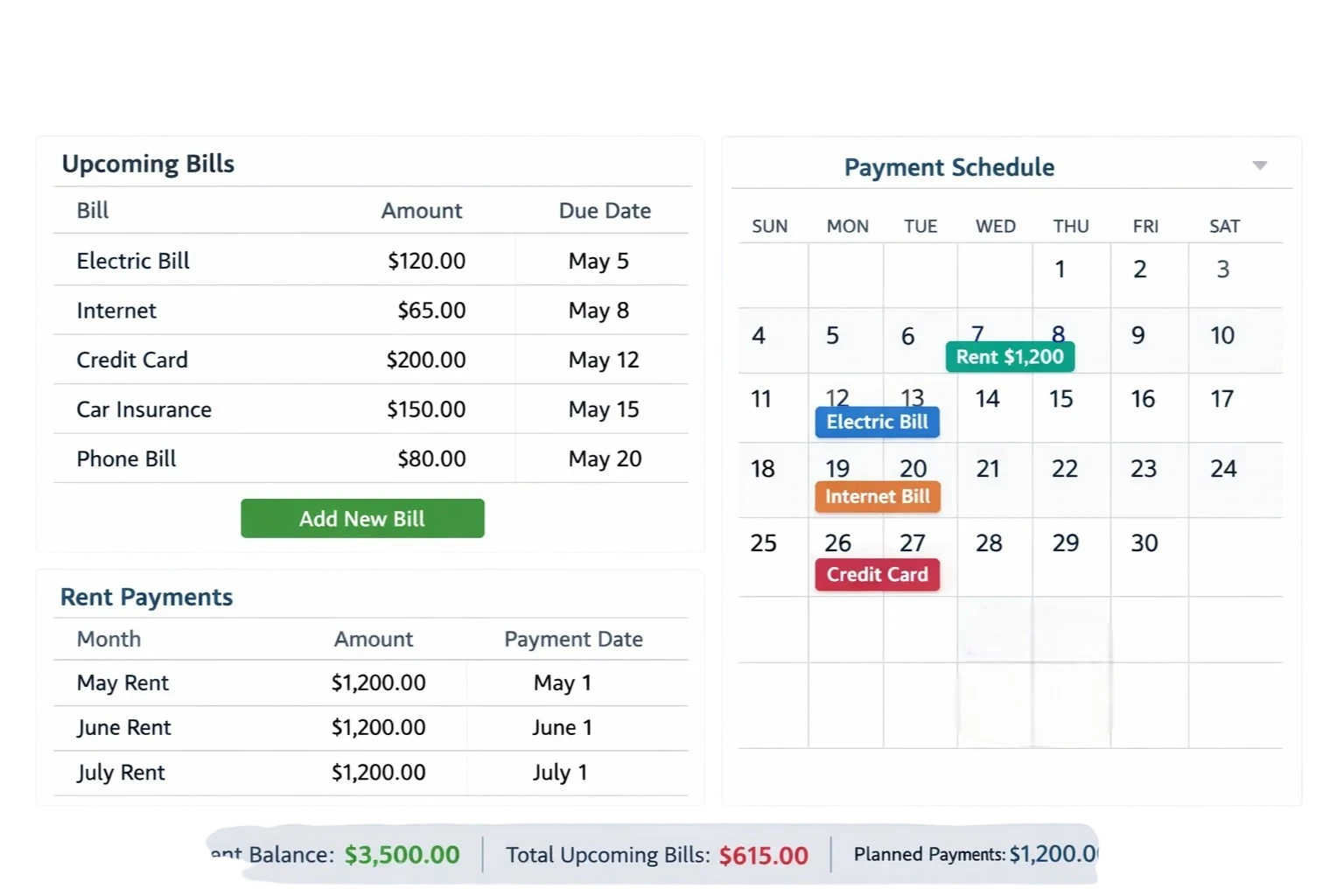

Misunderstanding Cash Flow

There’s a big difference between profit and cash flow. You might have a month where you sign multiple listings, close several deals, or fill vacant rental units, and show a lot of money on paper, but if the cash isn’t in the bank to pay your rent, your business is in trouble.

Many businesses run into problems because they don’t account for the timing of cash coming in and going out. They pay for supplies and labor today, cover staging, repairs, mortgage payments, insurance, or property taxes, but don’t get paid until closing or until rent is collected.

Note

To fix this, you need a cash flow forecast. This is just a simple way to look at when money is expected to come in and go out. By looking ahead, you can spot slow periods before they happen.

You might decide to delay a big equipment purchase or push a little harder on collections to make sure you have the cash to keep the business running.

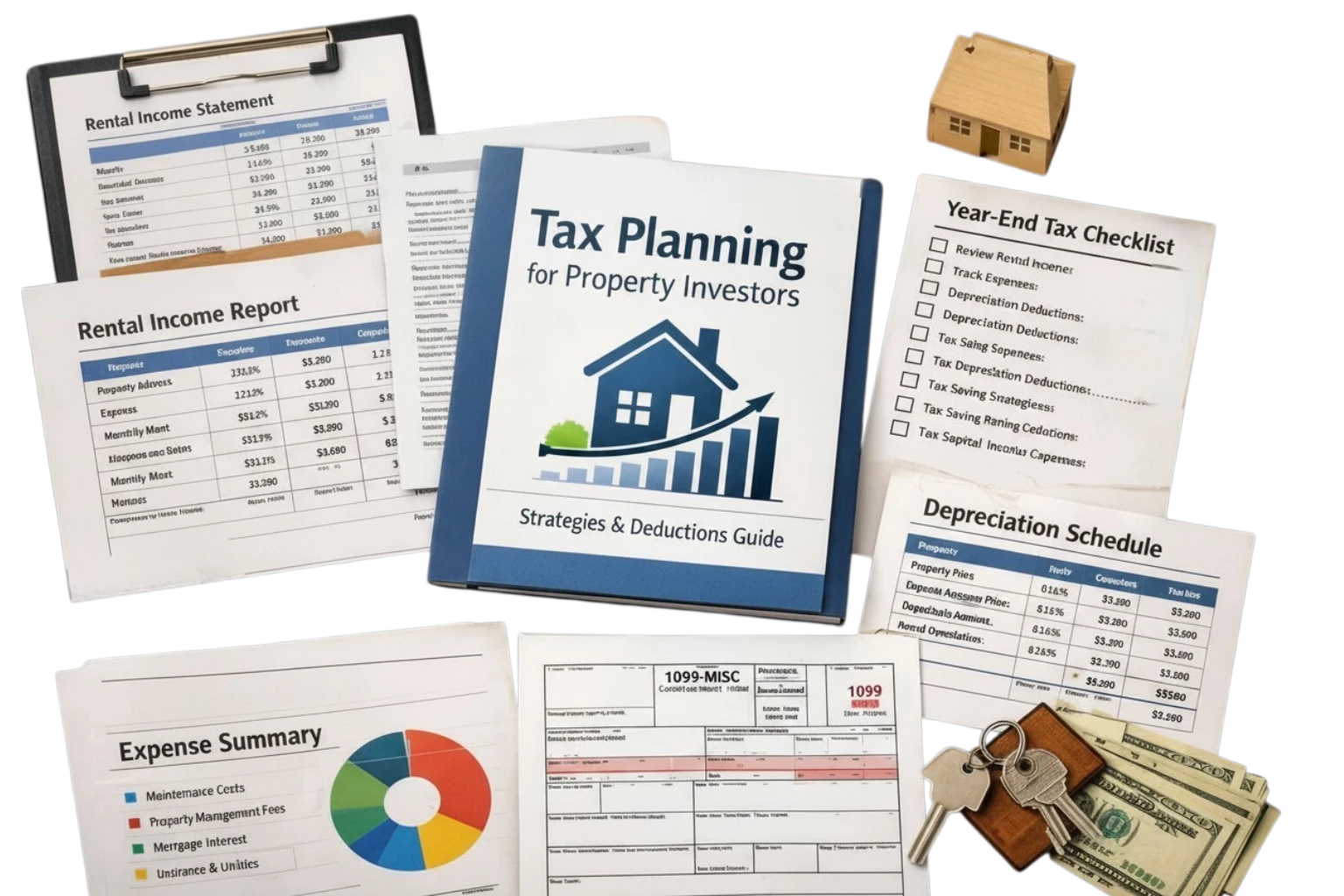

Not Planning for Taxes

Tax season should never be a surprise. Yet, every year, many small business owners are blindsided by a tax bill they didn’t save for. When you’re an employee, taxes are taken out before you ever see your paycheck. When you’re the boss, that responsibility falls entirely on you. If you spend every dollar that hits your account, you’re spending money that should have been set aside for taxes.

The best practice is to set aside a percentage of every payment you receive. Putting part of your gross income into a separate tax savings account helps ensure you’re prepared when taxes come due. It’s much easier to save a little bit as you go than to find $5,000 or $10,000 all at once.

This matters even more in real estate, where income may come in unevenly through commissions, rental income, short-term rental bookings, or property sales. Owners should also prepare for property taxes, self-employment taxes, capital gains considerations, and depreciation-related reporting when applicable.

Avoiding the Numbers

Perhaps the biggest reason for financial problems is simple avoidance. Many people feel anxious when they look at their spreadsheets. They worry the news will be bad, so they don’t look at all. That habit only makes the problems grow. Financial issues don’t go away because you ignore them. They only get more expensive to fix.

Note

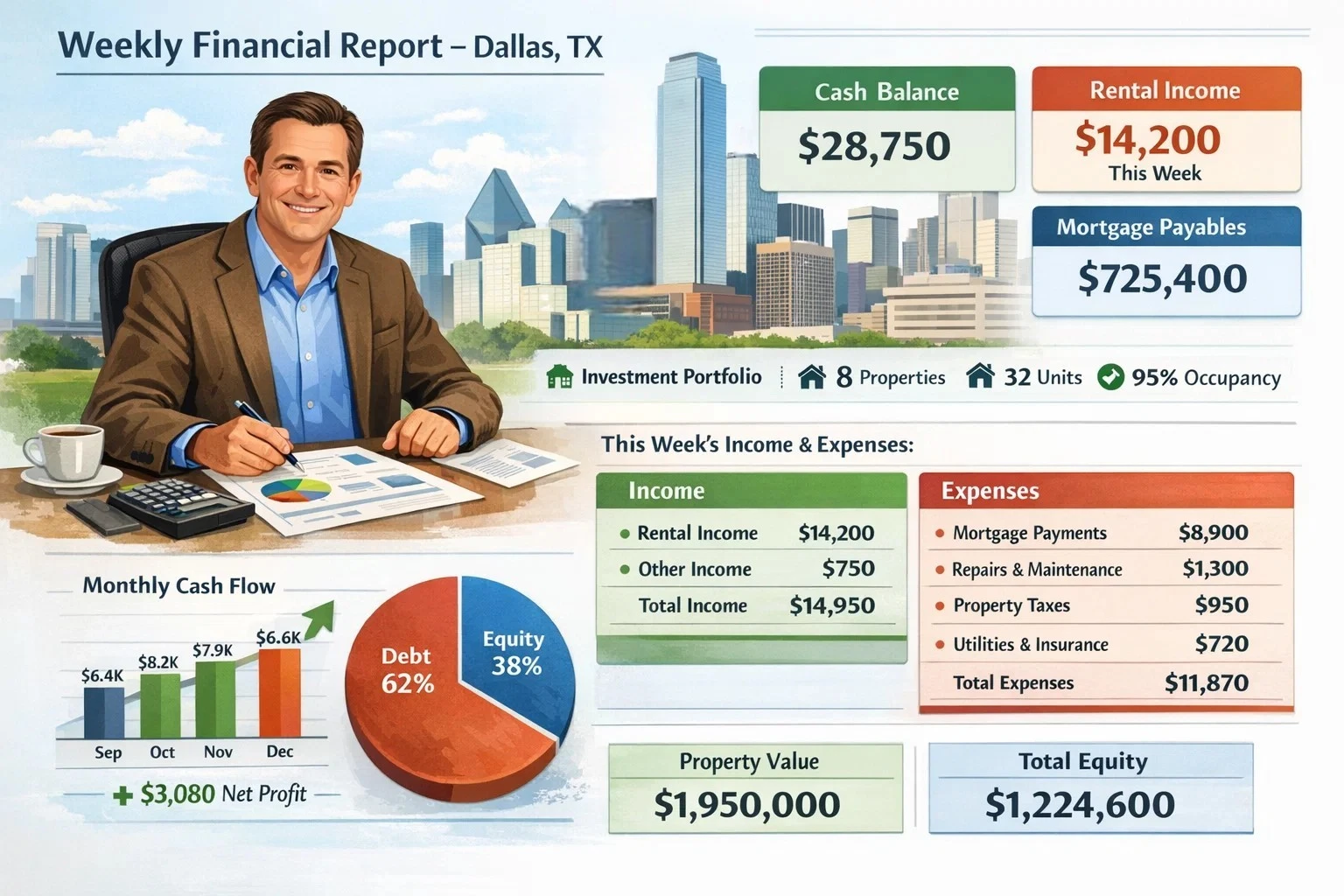

Do a weekly money check-in. Set aside 30 minutes every Friday to review your accounts, send out invoices, pay your bills, check rent collections, review vacancy costs, and monitor repair spending across properties.

When you look at your finances every week, the numbers lose their power over you. They become just another tool in your toolkit. You start to see patterns, catch errors early, and begin to feel a sense of control you didn’t have before.

Building a Business That Can Grow

Managing your money right isn’t just about staying out of trouble. It’s about creating a business that has value. If you ever want to take out a loan, bring on an investor, buy another property, refinance an existing one, or sell your company, you’ll need clean, organized books. You’re not just tracking pennies. You’re building a track record of success.

By putting these systems in place now, you’re giving your business the room it needs to grow. You’re moving away from guesswork and becoming an owner who runs the business with confidence and control. It takes discipline, and it might feel tedious at first, but the freedom that comes with financial clarity is worth it for any small real estate business owner.

{kind=link}