In a new national survey of renters, almost everyone dreams of home ownership, but affording it is not an option for many.

In Dallas, 97 percent of respondents claimed they want to own a home, but only 63 percent of those individuals could afford a mortgage in the city. The survey of 6,000 renters was created by Zumper, an apartment rental search company.

“The main contributing factor to this discrepancy seems to be that home values in Dallas are outpacing wage growth,” said Tanguy Le Louarn, head of data science at Zumper. “Various for sale reports in the Dallas area show an increase in home prices around 10 percent in the last year, some even report up to the mid double digits. Meanwhile, the Dallas Fed report recently stated that there has been a slow down in wage growth as higher paying jobs are being lost to lower paying ones—Dallas wages cannot keep up with the increasing home values.”

In fact, in a third of the surveyed cities, under half of renters earned enough income to qualify for a mortgage.

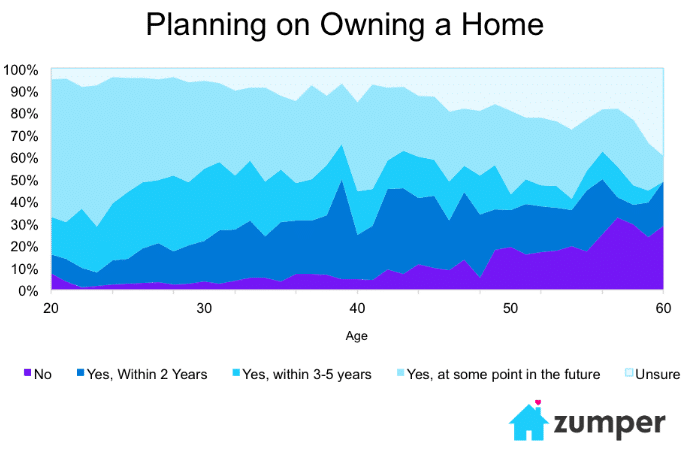

Interestingly, even though almost everyone surveyed wanted to buy, only 71 percent of respondents believe that the “American Dream” involves homeownership.

“While almost everyone wants to own a home at some point, the fact that only 71 percent of our respondents believe that the ‘American Dream’ involves homeownership highlights a potential shift in mentality of how this ideal can be achieved,” Le Louarn said. “While owning a home tends to be a good financial investment, it does not seem to be the end goal for as many people as it used to. Right now, homeownership is at its lowest ever and the renter population only continues to increase, especially among Millennials.”

As the report points out, since peaking in late 2005 at 69 percent, home ownership in the United States as reported by the Census Bureau has been on a steady decline, recently falling to a historical low of 62.9 percent during the second quarter of 2016. From 1965 to 1990, the homeownership rate averaged around 64 percent.

Part of the survey seems to indicate that certain renters don’t understand what involved with home ownership. For example, among the surveyed renters, their self-stated financial position had a minimal effect on their intention to buy a home. Approximately 90 percent of individuals who assessed their own financial status as “fair,” “good,” or “excellent” plan on purchasing a home.

Another example? Renters with student loans actually had a greater intention of eventually buying a home, 93 percent versus 87 percent of those who did not have loans. Of course, this could also indicate higher levels of education and therefore higher earning potentials among those with student loans. Ambition and ability are two different things.

While the majority of renters in quite a few cities indicated their intention to buy a home, the survey found that – based on the respondent’s self-reported incomes and the method used by Bloomberg to calculate the minimum salary required for a mortgage – many can’t afford a down payment.

It’s important to note the sample of 6,000 skewed younger than the general population, so the ability to afford a mortgage should rise if these people are able to sustain solid wage growth.

Perhaps as a way of saving up money toward a down payment, Millennials are taking on roommates. The survey found a whopping 62 percent of Millennials reported that they had at least one person with whom they shared their space. While these numbers may be partially impacted by the ages 20 to 23 population, who are often still in college and living with roommates, the figure was nearly 55 percent for those between the ages of 24 and 32.

{kind=link}